Nyhet —

OUTLOOK 2015: Stable but positive for fixed income in 2015

OUTLOOK 2015

Stable but positive for fixed income in 2015

Investors have enjoyed strong performance from across the bond asset classes in 2014. Government bond yields have fallen, while trends in credit markets have been mixed. Credit spreads tightened in investment grade but widened in high yield, although both asset classes have enjoyed solid absolute returns. Looking back, 2014 will likely be remembered for the growing divergence of monetary policy across regions.

Central bank policy is likely to dominate fixed income trends again in 2015 but we see three clear themes emanating:

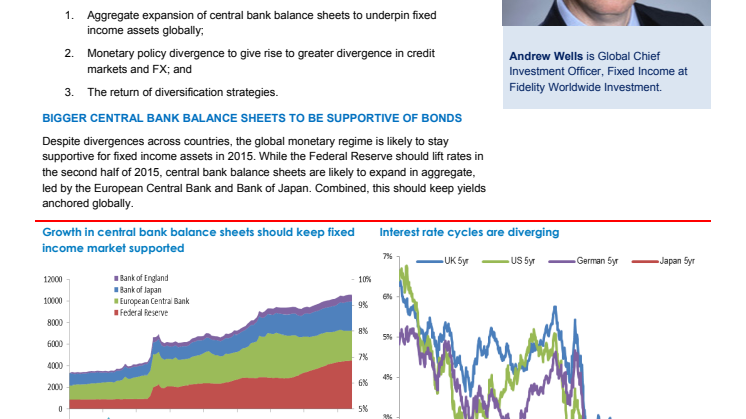

1. Aggregate expansion of central bank balance sheets to underpin fixed income assets globally;

2. Monetary policy divergence to give rise to greater divergence in credit markets and FX; and

3. The return of diversification strategies.

BIGGER CENTRAL BANK BALANCE SHEETS TO BE SUPPORTIVE OF BONDS

Despite divergences across countries, the global monetary regime is likely to stay supportive for fixed income assets in 2015. While the Federal Reserve should lift rates in the second half of 2015, central bank balance sheets are likely to expand in aggregate, led by the European Central Bank and Bank of Japan. Combined, this should keep yields anchored globally.

In the US, small rate increases are in the price and a significant pick-up in growth and inflation expectations will be needed to push bond yields materially higher. History provides useful case studies on how markets may react to such interest rate changes, but typically the worst falls in government bonds occur before the onset of tightening. 2013 was likely that period.

Ultimately, when the Fed looks to lift rates, it will be gradual and increasingly reactive to the bond market. Any rise in rates accompanied by aggressive spikes in longer-dated yields and credit spreads will be viewed as a threat to the economy. Indeed, policymakers will seek to minimise the risk of adverse market volatility. With many doves on the FOMC, such a cautious approach suggests that there are still good chances that US interest rates will even stay on hold in 2015. But this would only give rise to increasing concerns about the Fed getting behind the curve.

We expect inflation to stay low in 2015, but rising US wage pressures is the key risk to our view. The US and UK are at the front of the global cycle and eroding spare capacity will require close monitoring. A benign wages environment should see rates stay low for longer. Indeed, there is a risk that markets have underestimated globalisation trends and the increased labour market flexibility that may have watered down the link between growth and wages. Falling commodity prices could exacerbate these disinflationary trends.

However, ageing populations, shrinking US labour force participation and falling unemployment all suggest that wage pressures may be just around the corner. And with bloated central bank balance sheets, one shouldn’t underestimate the risk of a sharp turnaround in inflation dynamics and central bank policy. The challenge for investors is that markets will price this in well in advance of the onset of inflation. Therefore, with inflation premiums depressed, inflation-linked markets present a unique investment opportunity for 2015.

INTEREST RATE DIVERGENCE TO DRIVE CREDIT AND FX MARKET DIVERGENCES

In credit, the market is becoming less driven by fundamentals and more technically driven. Central bank policy is underpinning investor demand, making the market susceptible to the whims of sentiment. In late 2013 we argued that the hunt for yield would continue and we believe conditions are again ripe for this trend in 2015, particularly as policy rates stay relatively anchored.

More subtly, 2015 is likely to see increasing divergence across credit markets and there are early signs of widening differentials between EUR and USD spreads. In Europe, supportive monetary policy should provide strong tailwinds for euro credit. The ECB’s eagerness to expand its balance sheet should keep yields and spreads depressed and there are strong chances of QE involving both corporate and government bond purchases. For euro credit investors, there are opportunities for ongoing spread compression and Japan provides an extreme example of just how low spreads can go in the face of central bank support. But there are also good fundamental drivers with European companies more cautious than their US counterparts and periphery debt likely to recover further.

In the US, the credit cycle is in a mature phase. Talk of rate increases will keep sentiment more cautious, but we expect this to be transitory. Historically, it is not unusual for credit markets to falter in the early phases of tightening, but this is typically short-lived. Credit spreads and rates are negatively correlated and rising rates typically accompany spread tightening as economic conditions stay favourable. Indeed, current spreads are above the levels seen before the onset of many previous cycles, so we believe there is still scope for spread compression in 2015.

For FX markets, monetary policy divergence is likely to manifest through greater shifts in currency. Renewed efforts by the ECB and BoJ to increase the size of their balance sheets will put their currencies under the microscope. But competitive devaluation is a zero sum game for the global economy and quantitative easing is testing the limits of central bank credibility. While volatility in currency markets is low historically, investors shouldn’t underestimate the risk of spikes in 2015.

BACK TO BASICS – GETTING MORE OUT OF DIVERSIFICATION

The contrast between returns in 2013 and 2014 was stark. But there was a clear lesson from both periods. Macroeconomic forecasting is notoriously difficult to base investment decisions upon and diversification strategies are the best way to generate consistent returns. And faced with an incredibly high level of macro uncertainty, the market is highly sensitive to changes in the macro landscape – particularly growth, wages and inflation.

In late 2013 we warned of the consequences of reducing duration, which typically comes at the expense of increasing credit risk and correlation to risky assets. 2014 reminded investors that short-duration strategies are by no means a panacea. Indeed, precise market timing is required as otherwise the persistent income sacrifice erodes returns.

Entering 2015, it’s again tempting to reduce duration with 10-year Treasury yields at 2.4% – 60 basis points below where they were at the start of 2014. Instead, investors should use diversification as a primary means of managing interest rate risk. This can include blending the sources of duration across markets to capitalise on economic cycle divergences, which helps to preserve both income and diversification benefits. And while yields are low, so too are inflation premiums, so using inflation-linked bonds as a substitute for nominal duration is another way to temper the inflation and interest rate sensitivity of a portfolio.

Investment grade credit is still the sweet spot for bond investors, providing offsetting risks of duration and credit to underscore a more balanced return. But in the absence of a recession, high yield should continue to outperform and the widening of high yield spreads since the summer has provided an important valuation reset. While fundamentals are deteriorating, led by the US, interest cover ratios are high and there is little imminent refinancing risk, so the default environment is likely to stay depressed.

With the hunt for yield still in full swing, emerging market bonds should be a key beneficiary, offering optically striking yields versus most other areas of fixed income. Asia has an increasing role to play as part of this. Indeed, China RMB bonds have been a standout performer in 2014, up by more than 3% year to date, while exhibiting much lower volatility than the rest of the EM bond universe. Offering yields in excess of 4% with investment grade risk, it is an alluring proposition and powerful diversifier.

Liquidity is a primary concern for investors as thin markets can lead to more volatility. But this reflects both a risk and opportunity. Instead, investors need to segment their liquidity needs, capitalising on illiquidity premiums, while also ensuring adequate portfolio liquidity to meet cash needs. Liquidity is poorest in the most-yielding segments of the market where bid-offer spreads are widest and deal sizes are small – areas such as high yield, emerging market debt and esoteric segments such as financial hybrids. Therefore, barbell strategies that combine these asset classes with highly liquid segments can be a sensible investment strategy.

Overall, the key risks for fixed income in 2015 are economic – falls in growth and inflation are likely to support government bonds but to the detriment of credit, and vice versa. And it is hard to fathom credit spreads gapping wider in the absence of economic weakness and/or a material pullback in risky assets globally. The two go hand in hand. Thankfully, we expect the global economy to exhibit another year of economic muddle-through. This should underpin a stable but positive environment for fixed income in 2015.

Important information

This information is for Investment Professionals only and should not be relied upon by private investors. It must not be reproduced or circulated without prior permission.

This communication is not directed at, and must not be acted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required.

Fidelity Worldwide Investment refers to the group of companies which form the global investment management organisation that provides information on products and services in designated jurisdictions outside of North America. Fidelity Worldwide Investment does not offer investment advice based on individual circumstances. Any service, security, investment, fund or product mentioned or outlined in this document may not be suitable for you and may not be available in your jurisdiction. It is your responsibility to ensure that any service, security, investment, fund or product outlined is available in your jurisdiction before any approach is made to Fidelity Worldwide Investment. This document may not be reproduced or circulated without prior permission. Past performance is not a reliable indicator of future results. Unless otherwise stated all products are provided by Fidelity Worldwide Investment, and all views expressed are those of Fidelity Worldwide Investment.

Fidelity, Fidelity Worldwide Investment, the Fidelity Worldwide Investment logo and F symbol are trademarks of FIL Limited. Fidelity only offers information on products and services and does not provide investment advice based on an individual's circumstances.

Issued by FIL Investments International (FCA registered number 122170) a firm authorised and regulated by the Financial Conduct Authority, FIL (Luxembourg) S.A., authorised and supervised by the CSSF (Commission de Surveillance du Secteur Financier) and FIL Investment Switzerland AG, authorised and supervised by the Swiss Financial Market Supervisory Authority FINMA.

IC14/107

Ämnen

- Finans