Blog post -

Fintech: Innovate Before it’s Too Late

Good afternoon

Our client Mark Loane, CEO of C5 Alliance has published a blog titled 'Fintech Innovate Before it's Too Late'. Mark explores the ramifications of cryptocurrencies and other financial technology for Jersey.

I wonder if you might find any of these suggested, possible angles useful to expand on the story, or develop the content further:

- Extremely topical with the recent Bitcoin announcement and Jersey’s first fintech conference, Mark explores the ramifications of cryptocurrencies and other financial technology for Jersey

- Following the innovation review we can see that Jersey’s GVA is dropping - the future of Jersey’s economy lies in finding innovative solutions. Fintech is a natural part of this mix, given our already strong financial sector and growing digital skills base

- Fintech is disrupting the financial sector - the core pillar of Jersey’s economy. Mark explores what we can do to successfully adapt to this new reality and generate growth and jobs

Please do not hesitate to contact me should you have any questions, or wish to arrange for press comment with Mark Loane.

Best

Emily

emily@marcom2.com

01534 631213

Blog Post:

Slowly but surely, fintech is transforming finance at a fundamental level. To stay relevant and competitive, Jersey must take a long-term, nuanced approach in embracing this reality.

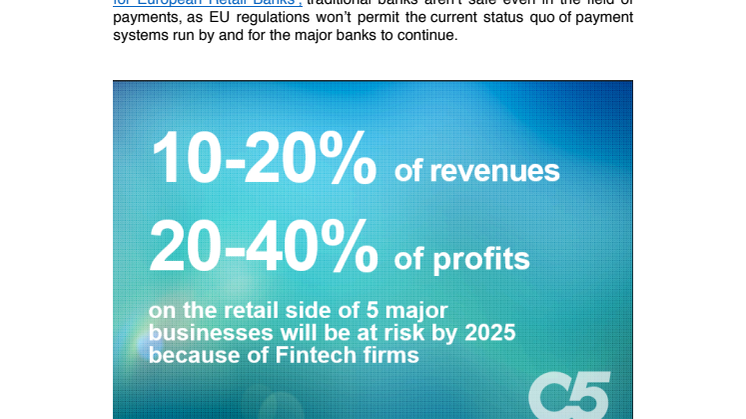

In their annual banking review, McKinsey predicted that 10% to 40% of revenues and 20% to 40% of profits on the retail side of 5 major businesses will be at risk by 2025 as a direct result of fintech firms’ market impact. According to a recent report from Deloitte, ‘The Emerging Challenge for European Retail Banks’, traditional banks aren’t safe even in the field of payments, as EU regulations won’t permit the current status quo of payment systems run by and for the major banks to continue.

The fact remains however that finance is one of the rare sectors that is still relatively untouched by disruptive technology – and irrespective of what certain voices from the fintech sector are claiming, established financial institutions aren’t going to be toppled overnight by fintech startups. Customers are still trusting established, robust banks and financial services that have weathered financial crises over new fintech companies.

The key thing to consider though is the long-term future of the finance sector; fintech companies are hiving off ancillary banking services, particularly in retail banking, as part of a slow but sure encroachment on financial services. The banks and other established financial institutions won’t collapse as a result of this, but their profitability will be significantly reduced in the coming years unless they take proactive, forward-thinking steps now.

The conservatism that we see from financial institutions is understandable given they’re concerned about their reputation and meeting regulatory standards. These institutions have positioned themselves in the marketplace as trustworthy places where people should feel safe putting their money. Following the financial crash, financial institutions have had to work hard to regain people’s trust – so any innovations will need to align with this strategy.

Couple this risk aversion with the sheer size of these financial institutions, and you can see why change and innovation is difficult to implement, even if the will is there. What’s important now is an appreciation at board level that if they don’t innovate, their competitors will, and that it’s possible to responsibly manage risk alongside implementing innovation. The positive thing is that it’s not too late.

The reality is that fintech solutions are often providing a higher quality service to customers. They can be faster, cheaper and more efficient – see TransferWise for example, which is already bypassing banks’ grip on foreign exchange, and the increasing popularity of Peer to Peer lending.

While most financial institutions do have innovation centres exploring the whole range of fintech solutions from new payment to mobile apps, these centres aren’t only experiencing issues with sluggish internal bureaucracy, they are also under-invested in comparison with fintech startups. Deloitte estimates that banks only account for 19% of an estimated $10bn in overall fintech investment in 2014, with non-banks accounting for 62%, and the rest coming from collaborations.

The reluctance or inability of legacy financial institutions to innovate their sector means we need a range of new solutions to deal with all the ramifications of fintech. Fintech goes beyond companies dealing directly with money, such as online payments or money transfers, to incorporate tech businesses which specialise in anything from customer services, project management and logistics, to automation and process. Machine learning is another huge area that will revolutionise financial services. Ultimately, fintech should be used to make financial companies more efficient and improve the overall quality of financial services. In the area of risk assessment for example, financial institutions can benefit from the data-driven lending that fintech enables.

It’s important that financial services in Jersey understand the magnitude of what fintech is doing to their sector, and then take a proactive approach to dealing with this reality. In Jersey especially, we have a unique window of opportunity to get all the right people in the room – regulators, financial experts, technologists and legal experts – to drive through agile, responsible and innovative change.

Our size is our advantage here – and we have other examples we can look to. Israel, which is about the size of Wales, is a global powerhouse for fintech with over 200 fintech startups. With a limited local market in Israel, the fintech industry there focusses on larger global markets, using their base as a test market. Crucially, established financial institutions in Israel invest a significant amount in fintech technology, and the country has a clear, government-led innovation strategy. If Jersey followed suit, we would have even more opportunities, given our greater direct access to many major international financial firms. Our technology services in Jersey are already providing world-class solutions to international clients in finance. If financial services in Jersey want to embrace fintech, they have access to all of the resources they need right here.

When it comes to fintech, we can and do experience myopic and extreme thinking from both sides – in the financial world where technology is seen by some as encroaching on a world it has no right to be in, and in the technology world, where some see established financial practices as useless and archaic. The truth is somewhere in between; it’s possible and desirable to effect a synergy between finance and technology, ignoring both the reactionaries and the hype. We’ve all lived through several major disruptions from technology, for example internet banking in 2001, so we mustn’t lose our heads, but we also can’t afford to do nothing.

We can see in the image above that Jersey’s GVA is dropping. Unless we take innovation seriously, this trend will continue.

A particular motivation for innovation in financial services is the development in Blockchain technology. This is making cryptocurrency a force which could change the very nature of the financial sector by taking out banks as an intermediary.

In 5 years, the global finance sector will be unrecognisable. The power is shifting more and more away from established institutions to the individual customer. Whether this is a threat or an opportunity for Jersey’s financial services depends on what they do – or fail to do - now.

View the Blog post online here

Related links

Topics

- Data, Telecom, IT

Categories

- jersey

- fintech

- digital jersey

- channel islands

- c5 alliance