Press release —

Home or car expenses, and short-term debt, are the top two reasons for Two-Pot withdrawal requests

Discovery Corporate and Employee Benefits reveal Two-Pot eligibility data as well as rates and reasons for withdrawal requests

30 September 2024

In line with industry expectations that debt repayment would be a key reason for requesting Two-Pot withdrawals, one of the two main reasons claimants gave for needing extra cash was to settle short-term debt. The other was to cover home or car expenses.

This is according to the Discovery Corporate and Employee Benefits’ pension and provident fund business. They represent over 3,000 employer groups and just over one million employees, and asked claimants for reasons why they had chosen to withdraw from their accumulated retirement savings as part of the new Two-Pot retirement system.

Guy Chennells, Chief Commercial Officer at Discovery Corporate and Employee Benefits explained that the data was gathered from individuals who submitted withdrawal requests via a user-friendly WhatsApp channel.

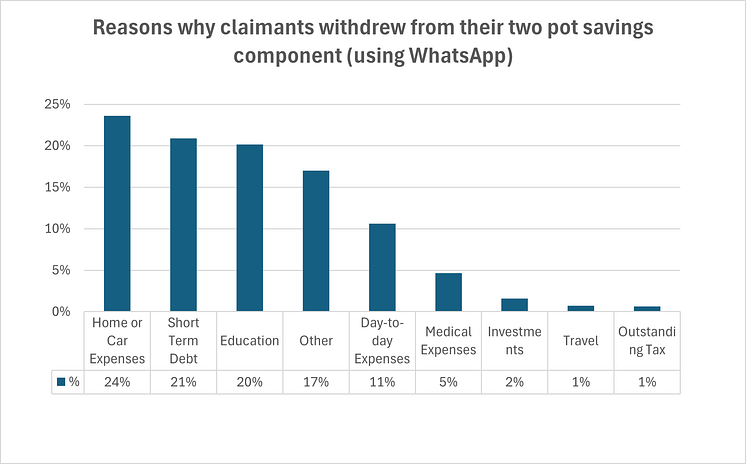

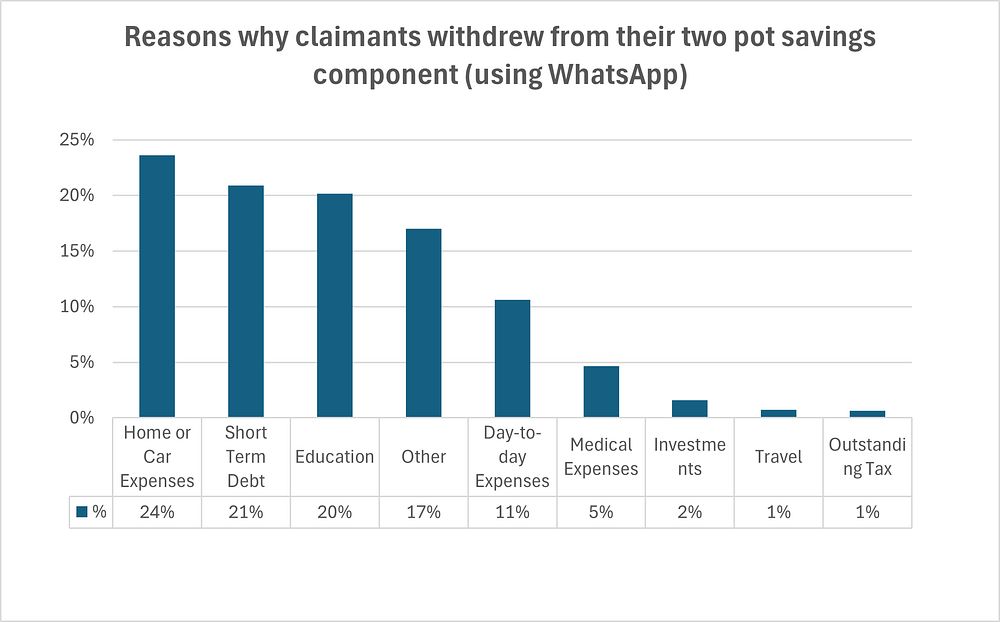

“Responses showed that the main reason our claimants withdrew from their savings was to resolve home or car expenses (24%). This was closely followed by a need to pay off short-term debt (21%),” he said. “We found it surprising that a big group of claimants (20%) was using the extra money for education, presumably in the majority of cases for children’s school fees, as well as for day-to-day expenses (11%). Sadly, these are all indications of the cost-of-living crisis faced by so many,” he said.

The Two-Pot retirement system was implemented in September 2024 mainly to help South Africans stay invested in their retirement funds until they retire. The system gives individuals access to one-third of their retirement savings for short-term needs while preventing them from withdrawing from their retirement fund in full when changing jobs.

Source: Discovery Corporate and Employee Benefits (16-27 Sept 2024)

Chennells explained that if claimants chose the ‘Other’ category as their Two-Pot withdrawal reason, were asked to give a written example of what ‘Other’ meant for them.

“While a notable 17% of claimants selected ‘Other’ as their motive for withdrawal, the majority of reasons given here was for home improvements and renovations,” he says. “This isn’t really recommended as a good use of Two-Pot savings because it does not truly classify as ‘emergency spending’. It’s still understandable, though, because South Africans who want to improve their lives are simply unable to create discretionary spending from their regular income at the moment.”

Travel was only selected as a reason for withdrawal from Two-Pot savings by 1% of claimants. This is a good sign that the majority of individuals were not accessing their Two-Pot savings for a whimsical escape to the beach or bush.

Withdrawal rates and preferred channels vary notably by income group

“Building an automated payment process that doesn’t require any manual intervention has been a key focus of ours, to ensure members can access these funds when they need to, in a convenient and seamless way,” notes Chennells.

“We built a secure web and app journey and robust WhatsApp channel to make the process simple and extremely user friendly. As a result, our team was able to process 180 times our usual daily claim volume during the first day of Two-Pot claims,” he continues. “We’re exceptionally pleased that we have been able to process payments quickly for our clients, with 29% paid within three days of claim submission, 84% within four days, and a 99% within five days of submission.”

“We found that approximately 75% of people chose the web or app route for submitting their withdrawal requests. This is a testament to the high rate of digital engagement by Discovery Retirement Fund members. This channel did not seem to vary much by age at all,” Chennells says.

He adds that the channel claimants chose to use did vary by income, however, with 40% of the low-income group using WhatsApp. This decreased to only 8% of very high-income members.

People between 35 and 45 years’ old, have highest Two-Pot claims rates

Discovery’s Corporate and Employee Benefits team has recorded that, of those claimants who were eligible to withdraw, a total of 22% of the total eligible retirement fund member base have opted to make a withdrawal during September. Of this total, if we were to split our middle-aged people into two separate age groups of 35 and 45, as well as 45 and 55, we note that those individuals who are aged between 35 and 45 years old have taken the highest total number of withdrawals from their accumulated retirement savings (27% of those eligible).

“This figure emphasises the pressures facing South Africa’s ‘sandwich generation’, who are battling to support young children while potentially being responsible for their older parents too,” adds Chennells. “This is worsened by the recent high-inflation cycle, increased debt and electricity costs and other cost-of-living pressures which have devastated household finances, especially for families.”

Of the 22% of total withdrawals recorded during September, it’s interesting to note the range of withdrawal rates that Discovery’s Corporate and Employee Benefits’ data set highlights a range: From over 40% for those who are middle-aged with a low- to medium-income (low: R0 to R125,000 per year; medium: R125,000 to R500,000 per year), to less than 1% for those individuals over 55 years old who also had very high income (over R1 million per year).

“By age alone, withdrawal rates were similar for the young and middle-aged (around 25%), but about half that for the over 55 group (13%),” says Chennells. “Income was a much stronger driver of withdrawal rates with low-income claimants at 38%, middle-income at 29%, high income at 12%, and very high-income claimants at just 4%.”

A handful of claimants experienced challenges because as a result of small errors in the details. For example, William was spelled ‘Willliam’ (with an extra ‘l’), causing the Home Affairs verification system to reject an application.

“Discrepancies between details on our system compared with the employers’ or SARS systems also caused a few problems,” says Chennells. “But these learnings have helped us grow building new rules into our systems to avoid any future hold-ups.”

Qualifying for withdrawal in the Two-Pot retirement system after 1 September 2024

Chennells cautions that withdrawal rates during September should be understood within the context that many people did not qualify for a withdrawal for two key reasons:

- If there was less than R2000 in their savings account from the seeding, claimants were not allowed to withdraw; and

- If claimants are in the over-55 age category, they must physically opt in to the Two-Pot regime before 1 September 2025 for their seeding to occur.

The data revealed that claimants’ eligibility to make a Two-Pot withdrawal was different by age and income.

By age, 45% of those below 35 qualified in September, 71% of those between 35 and 55 (middle-aged) qualified, and 61% of those over 55 were eligible. For those over 55, a further 20% would have enough savings to qualify if they opted in (which they are able to do before September 2025).

By income the data is even more stark. Of those earning R125,000 per year or less (low-income), only 34% were eligible.

“As this is the group with the highest claiming rate, withdrawals overall would have been much higher without the R2000 minimum requirement,” notes Chennells. “It also means that withdrawals are expected to rise by the end of the year as savings components grow with contributions and investment returns.”

Of the middle-income group (R125,000 to R500,000 per year), 67% qualified, while 83% of the high-income group (R500,000 to R1 m per year), and 90% of the very high-income group (above R1 m per year) qualified.

Guidance and advice works

Even though the daily withdrawal volumes recorded were so much higher than usual from 1 September, only 22% of Discovery Corporate and Employee Benefits’ members who qualified to withdraw have done so, to date.

“So far, Two-Pot withdrawals have been lower than our team expected, and we hope that some of this is due to people changing their minds about dipping into their retirement savings,” says Chennells. “Understanding other options for short term capital, or how much more you will have to contribute to your fund later if you withdraw, or how much you will lose to tax, has proved critical in helping people make the right decisions.”

“There might be another spike in withdrawals in November during Black Friday, possibly another at Christmas and a third early next year, as the new school year starts. However, the relatively low percentage of overall withdrawals shows that most people understand they must only draw on their savings pots in genuine financial emergencies. They realise that the more disciplined you are about not withdrawing, the more you will have available if one day you really do need it”, Chennells concludes.

Topics

Categories

Discovery information

About Discovery

Discovery Limited is a South African-founded financial services organisation that operates in the healthcare, life assurance, short-term insurance, banking, savings and investment and wellness markets. Since inception in 1992, Discovery has been guided by a clear core purpose – to make people healthier and to enhance and protect their lives. This has manifested in its globally recognised Vitality Shared-Value insurance model, active in over 40 markets with over 40 million members. The model is exported and scaled through the Global Vitality Network, an alliance of some of the largest insurers across key markets including AIA (Asia), Ping An (China), Generali (Europe), Sumitomo (Japan), John Hancock (US), Manulife (Canada) and Vitality Life & Health (UK, wholly owned). Discovery trades on the Johannesburg Securities Exchange as DSY.

Follow us on Twitter @Discovery_SA