Nyhet -

China pulls support levers as growth slows

As economic activity in China slows, the authorities have signalled their intent to support growth with rate cuts and policy stimulus. By historical standards, Chinese stocks remain relatively cheap and investors should not underestimate the amount of levers China can pull to offset downward pressures. In the short-term, the property sector will likely benefit from rate cuts although investors should continue to keep their eye on the long-term beneficiaries of China’s move towards a more domestic-consumption driven economy.

QUALITY OF GROWTH

Most investors in China will be familiar with the long-term fundamental drivers: one of the highest GDP growth rates in the world, consistent earnings growth, increased urbanisation, a growing middle class, growing domestic consumption, vast infrastructure spending and the potential for dozens of under-penetrated sectors to grow on the back of the biggest population on the planet. In recent times however, investors have had to come to terms with annual growth rates that have slipped from the double-digits to a more prosaic 7-8%. This partly reflects external uncertainties, such as the Euro-zone sovereign debt crisis and concerns over stuttering US growth and the “fiscal cliff”, but it’s also a reflection of a change in emphasis by China’s leadership.

After formally reducing their growth target for 2012 to 7.5% from 8%, it appears that China’s leaders are content to settle for more balanced, higher quality growth and to turn away from the export-led sprint of the past decade. However, after a spate of weaker economic data the authorities now appear ready to support growth and they have far more scope to do this than their counterparts in the US and Europe. But the authorities will be reluctant to launch a massive round of fiscal stimulus as they did in the wake of the 2008 Lehman bankruptcy, for fear of touching off another inflationary spiral.

TESTING TIMES

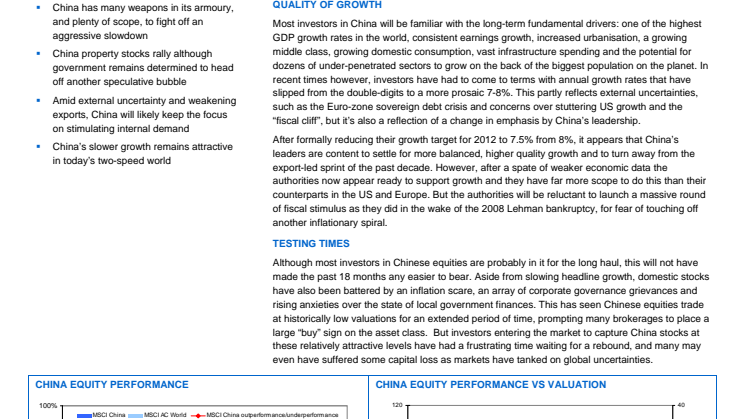

Although most investors in Chinese equities are probably in it for the long haul, this will not have made the past 18 months any easier to bear. Aside from slowing headline growth, domestic stocks have also been battered by an inflation scare, an array of corporate governance grievances and rising anxieties over the state of local government finances. This has seen Chinese equities trade at historically low valuations for an extended period of time, prompting many brokerages to place a large “buy” sign on the asset class. But investors entering the market to capture China stocks at these relatively attractive levels have had a frustrating time waiting for a rebound, and many may even have suffered some capital loss as markets have tanked on global uncertainties.

EXTERNAL THREATS, INTERNAL PRESSURES

The relative underperformance of Chinese stocks in recent times can be explained in part by external volatility (likely to persist for some time) but also by last year’s domestic inflation scare that saw one-year lending rates ratcheted up to 6.56%, placing strains on smaller companies, non-performing loan ratios at banks and wider economic activity. But many analysts now appear confident that China will avoid a hard landing unless the Euro-zone (China’s largest trading partner) comes apart in dramatic fashion. Moreover with inflation now below 3%, China is wielding more of the weapons in its armoury to fight off a further slowdown.

The Chinese government signaled a more aggressive approach to sustaining expansion in May 2012 when Premier Wen Jiabao called for more efforts toward stabilizing growth. The People’s Bank of China on June 7 cut interest rates for the first time since 20081 and the economic planning agency has stepped up approvals of investment projects. Rates were reduced again July 5 in an earlier-than-expected move. The government has also reduced banks’ reserve requirements three times since November 2011. Analysts at Citigroup Global Markets expect more interest rate cuts to boost demand, two more RRR (required reserve ratio) cuts to bring money growth to 14%, expansionary fiscal policy within the limit of the budget, and targeted property policy easing to prevent an investment slump2.

Fidelity fund manager Raymond Ma says: “I remain confident that all these easing measures should filter through to generate an economic recovery in the coming quarters. Sector-wise, lower lending rates and higher lending rate discounts should no doubt help encourage more potential homebuyers to enter the property market.”

ECONOMIC DATA BRINGS GOOD AND BAD NEWS

Data from China in the first half clearly reflected a broad slowdown in economic activity, with trade and manufacturing indicators weakening on the back of external volatility, the effects of domestic monetary tightening in 2011, currency appreciation and rising labour costs. More recent data paints a mixed picture for China’s economy. China’s exports rose in May at more than double the pace analysts estimated, with overall shipments up 15.3% year-on-year3 as US demand for Chinese exports offset weaker shipments to Europe. However, industrial output and retail sales data trailed forecasts. Meanwhile, China’s consumer inflation slowed to the lowest level in almost two-and-a-half years in June, with the consumer price index up 2.2% from a year earlier and down from a rise of 3% in May4. This explains why the central bank has been comfortable with cutting interest rates twice in less than a month, and provides further scope for the government to ease policy. However, investors will not have been cheered by news that China’s imports rose a less-than-expected 6.3% in June and export growth slowed to 11.3%, widening the trade surplus to US$31.7 billion5. Overall, the data provides the backdrop for China’s recent actions to support growth, and Wen Jiabao has promised further fine-tuning of policies to offset downward pressures on the economy6.

PROPERTY RALLIES

Leaving broad economic statistics to one side, there have been tangible signs that China’s all-important property sector is improving. China home prices began to drop in 2010 as the government tightened policy to contain overheating, fueled by previous stimulus-driven investment. Policy measures were stepped up throughout 2011 as the government battled rising inflation, hitting related sectors such as construction and basic materials and growth in the wider economy. This year the government has signaled a modest change in direction, allowing local governments to support weaker areas of the market while keeping intact broader policies aimed at discouraging real estate speculation. So we have seen municipalities implement measures such as more flexible conditions for land grants, more favourable interest rates for first-time buyers and reductions in transaction-related taxes and fees.

As such, the China property market has shown signs of stabilization with incremental rises in home sales and house prices. According to the China Real Estate Index System (CREIS) operated by the largest China on-line real estate company SouFun Holdings, new home prices in 100 major Chinese cities rose in June, ending a nine-month decline7. Transaction volumes in the first half rose 19% year-on-year in first- and second-tier cities8, as a prolonged decline in prices tempted buyers back into the market. Amid ongoing global uncertainty and with inflation below 3%, there’s a strong chance the government will cut rates further. However, as Wen Jiabao said on July 7, China must make “controls against speculative housing demand a long-term policy."

Fidelity fund manager Stephen Ma says: “Sector-wise, real estate developers could be the key beneficiaries of the monetary easing cycle. Moreover, companies which are highly geared may also benefit from the interest rate cut. These companies may witness an upward earnings revision in light of the move. On the contrary, banks could be the key victims of the cut as their net interest margins (NIM) may be compressed accordingly and their earnings forecasts may also be downgraded.”

CONCLUSION

With China moving into a different phase of the economic cycle, the government is stepping up easing policies to support growth. Now that inflationary pressures have cooled down, the authorities have more freedom to support weaker areas of the economy while maintaining clamps on areas with a tendency to overheat. For investors, the key for China is not whether it can continue to grow at double-digit percentage rates, it's whether it can achieve more sustainable, balanced growth – and 7.5% in the two-speed world we're living in still remains attractive on a relative basis.

Sources:

- Bloomberg, 07.06.2012

- Citigroup Global Markets, “Focus on China”, 22.06.2012

- Reuters, June 2012

- WSJ, 09.07.2012

- Bloomberg, 10.07.2012

- Xinhua News, 08.07.2012

-

CREIS, Soufun, 02.07.2012

-

Morgan Stanley Research, “China Property Tracker”, 05.07.2012

This information is for Investment Professionals only and should not be relied upon by private investors. This information must not be reproduced or circulated without prior permission. This communication is not directed at, and must not be acted upon by persons inside the United Kingdom or the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. Fidelity/Fidelity Worldwide Investment means FIL Limited, and its subsidiary companies. Unless otherwise stated, all views are those of the Fidelity organisation. Fidelity only offers information on its own products and services and does not provide investment advice based on individual circumstances. Fidelity, Fidelity Worldwide Investment, and the Fidelity Worldwide Investment logo and currency F symbol are trademarks of FIL Limited. No statements or representations made in this document are legally binding on Fidelity or the recipient. Any proposal is subject to contract terms being agreed. We recommend that you obtain detailed information before taking any investment decision. Prior to making your investment, please ensure you have read the Key Investor Information Document (KIID) which is available along with the full prospectus, current annual and semi-annual reports free of charge from our distributors, from our European Service Centre in Luxembourg and from your financial advisor or from the branch of your bank. Past performance is not a reliable indicator of future results. The value of investments [and the income from them] can go down as well as up and investors may not get back the amount invested. For funds that invest in overseas markets, changes in currency exchange rates may affect the value of an investment. Foreign exchange transactions may be effected on an arms length basis by or through Fidelity companies from which a benefit may be derived by such companies. Issued by FIL (Luxembourg) S.A.(registered in Luxembourg), regulated in Luxembourg by the CSSF (Commission de Surveillance du Secteur Financier). SSL1207N06/0113

Ämnen

- Finans

Kategorier

- growth

- fidelity worldwide investment

- fidelity international

- fidelity

- china

- consumption