Nyhet -

Europas kärna hotas - vad händer om Frankrikes kreditbetyg nedgraderas?

Last week, S&P appeared to downgrade France from triple-A on its website – a change later confirmed as erroneous following a ‘computer glitch’. Error or not, the agency’s actions have nevertheless raised eyebrows among investors.

- France has vulnerabilities: its economy is slowing, it has the highest debt levels amongst triple-A eurozone nations and it has significant fiscal work to do on its balance sheet. It also has several large banks exposed to eurozone debts, which appear to be ‘too big to save’.

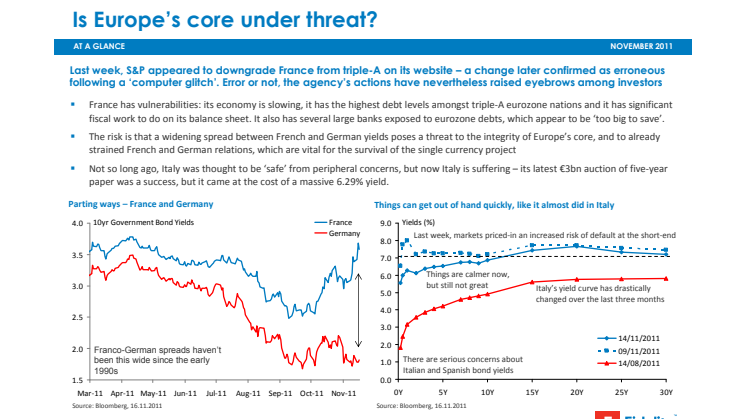

- The risk is that a widening spread between French and German yields poses a threat to the integrity of Europe’s core, and to already strained French and German relations, which are vital for the survival of the single currency project

- Not so long ago, Italy was thought to be ‘safe’ from peripheral concerns, but now Italy is suffering – its latest €3bn auction of five-year paper was a success, but it came at the cost of a massive 6.29% yield.

France’s triple-A rating is important

- France’s triple-A sovereign debt rating enables it to manage its public debt (due to peak at above 87% of GDP next year) and a downgrade would directly impact the European Financial Stabilisation Facility (EFSF), Europe’s €440bn bailout fund

- If France loses it triple-A status, it would put the EFSF’s own triple-A rating at risk – indebted eurozone members rely on the EFSF to access funding at much lower triple-A rates and France is the second-largest contributor

- Recent third quarter GDP results for France and Germany revealed that the eurozone core is still supporting modest eurozone growth, but fears of a looming eurozone recession remain, as the latest leading PMIs have dropped into contraction territory (see chart right)

- Its not just France’s rating that is being questioned – yields on Austrian and Dutch triple-A government bonds have also risen over downgrade concerns, leaving few safe havens for investors and the prospect of a shrinking eurozone core that comprises of only Germany.

Final thoughts

Investors will need to take a pragmatic, strategic approach to the way they manage their European equity and bond exposures

- Managing peripheral exposure will be vital, and certain financials may still have large exposures to these troubled regions – despite the promise of unlimited liquidity from the ECB, interbank lending and funding costs could cause further pain for banks

- Within equities, recessionary concerns may negatively affect the performance of cyclical stocks by a greater magnitude than defensive names, so it makes sense for investors to take a more defensive stance during these uncertain times; especially for higher-yielding companies with reliable earnings streams who are growing their dividends

- The key is to remain flexible and not forget the importance of income-producing assets in this low growth environment – bond investors would be wise to adopt a strategic approach to their investments, while equity investors should consider high-quality stocks with healthy dividend yields as a source of future total returns.

“A lack of real economic growth is a problem for over-indebted economies that remain reluctant to engage in serious debt restructuring. Investors remain highly sensitive to the political events unfolding in Europe as EU leaders try to restore confidence. The key is to remain diversified and in particular, not to be over concentrated in financials. Financials remain the largest source of volatility in the market since their abilities to operate are threatened by the risk of a eurozone sovereign debt fallout.“

Ian Spreadbury, Portfolio Manager, Fixed Income

“Savers needing income should look at equity markets. Even if equity markets are showing volatility in growth, equity funds can provide a good alternative source of income. For the last 20 years, investors have bought equity markets for capital growth, but now is the time to buy equities for income.”

Dominic Rossi, Global CIO, Equities

This information is for Investment Professionals only and should not be relied upon by private investors. It must not be reproduced or circulated without prior permission. This communication is not directed at, and must not be acted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. Fidelity/Fidelity Worldwide Investment means FIL Limited and its subsidiary companies. Unless otherwise stated, all views are those of Fidelity. Fidelity only offers information on its own products and services and does not provide investment advice based on individual circumstances. Fidelity, Fidelity Worldwide Investment, the Fidelity Worldwide Investment logo and F symbol are trademarks of FIL Limited. Growth Investments Limited is licensed by the MFSA. Fidelity Funds are promoted in Malta by Growth Investments Ltd in terms of the EU UCITS Directive and Legal Notices 207 and 309 of 2004. The Funds are regulated in Luxembourg by the Commission de Surveillance du Secteur Financier; Our legal representative in Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich. Paying agent for Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich.Issued by FIL Investments International (FSA registered number 122170) a firm authorised and regulated by the Financial Services Authority. FIL Investments International is a member of the Fidelity Worldwide Investment group of companies and is registered in England and Wales under the company number 1448245. The registered office of the company is Oakhill House, 130 Tonbridge Road, Hildenborough, Tonbridge, Kent TN11 9DZ, United Kingdom. Fidelity Worldwide Investment’s VAT identification number is 395 3090 35. SSO4641/1112

Ämnen

- Finans

Kategorier

- fidelity

- fidelity international

- fidelity worldwide investment

- finanskrisen

- kreditbetyg

- frankrike

- återhämtning