Nyhet -

Grekland klart för massiv skuldsanering

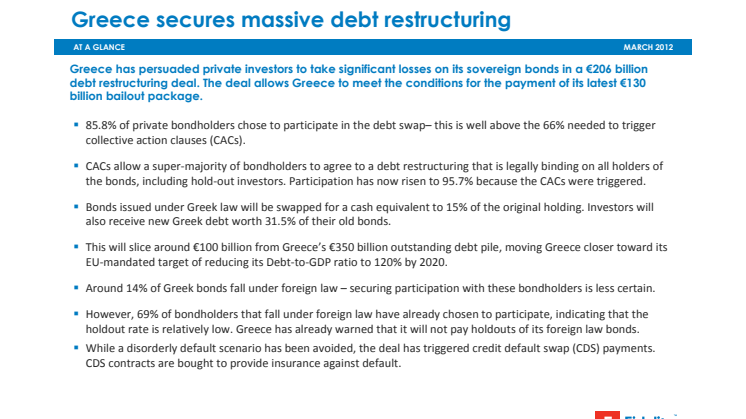

- 85.8% of private bondholders chose to participate in the debt swap– this is well above the 66% needed to trigger collective action clauses (CACs).

- CACs allow a super-majority of bondholders to agree to a debt restructuring that is legally binding on all holders of the bonds, including hold-out investors. Participation has now risen to 95.7% because the CACs were triggered.

- Bonds issued under Greek law will be swapped for a cash equivalent to 15% of the original holding. Investors will also receive new Greek debt worth 31.5% of their old bonds.

- This will slice around €100 billion from Greece’s €350 billion outstanding debt pile, moving Greece closer toward its EU-mandated target of reducing its Debt-to-GDP ratio to 120% by 2020.

- Around 14% of Greek bonds fall under foreign law – securing participation with these bondholders is less certain.

- However, 69% of bondholders that fall under foreign law have already chosen to participate, indicating that the holdout rate is relatively low. Greece has already warned that it will not pay holdouts of its foreign law bonds.

- While a disorderly default scenario has been avoided, the deal has triggered credit default swap (CDS) payments. CDS contracts are bought to provide insurance against default.

A default by any other name…

The ECB stopped accepting Greek bonds in liquidity operations after S&P declared Greece to be in “selective default” last week. The fact that Greece has triggered the CACs means that the International Swaps and Derivatives Association (ISDA) has treated the deal as a default that will trigger CDS payments. The restructuring eases the risk of contagion from Greece, but it is by no means the end of the eurozone debt crisis – other hurdles include ratifying the fiscal compact and raising the lending capacity of Europe’s bailout funds; the EFSF and ESM.

“The good news is this deal averts the risk of a hard default on the March bond maturity and it lowers future systemic risk from Greece since the share of post-PSI debt in private hands is cut. The bad news is Greece remains in a very difficult economic situation; a eurozone exit may still be on the cards if the second Troika program proves unworkable. German citizens have become increasingly opposed to further Greek bailouts, while anti-Troika sentiment is growing in Greece. There is some concern among bond investors that the deal might encourage policymakers to try similar PSI restructurings in other countries given the relatively muted market reaction. I hope that the halo effect from the LTRO has not bred complacency.”

Tristan Cooper, Sovereign Analyst, Fidelity Worldwide Investment

This information is for Investment Professionals only and should not be relied upon by private investors. It must not be reproduced or circulated without prior permission. This communication is not directed at, and must not be acted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. Fidelity/Fidelity Worldwide Investment means FIL Limited and its subsidiary companies. Unless otherwise stated, all views are those of Fidelity. Fidelity only offers information on its own products and services and does not provide investment advice based on individual circumstances. Fidelity, Fidelity Worldwide Investment, the Fidelity Worldwide Investment logo and F symbol are trademarks of FIL Limited. Growth Investments Limited is licensed by the MFSA. Fidelity Funds are promoted in Malta by Growth Investments Ltd in terms of the EU UCITS Directive and Legal Notices 207 and 309 of 2004. The Funds are regulated in Luxembourg by the Commission de Surveillance du Secteur Financier; Our legal representative in Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich. Paying agent for Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich.Issued by FIL Investments International (FSA registered number 122170) a firm authorised and regulated by the Financial Services Authority. FIL Investments International is a member of the Fidelity Worldwide Investment group of companies and is registered in England and Wales under the company number 1448245. The registered office of the company is Oakhill House, 130 Tonbridge Road, Hildenborough, Tonbridge, Kent TN11 9DZ, United Kingdom. Fidelity Worldwide Investment’s VAT identification number is 395 3090 35. SSO5117/0313

Ämnen

- Finans

Kategorier

- skuldsanering

- cds

- greece

- grekland

- fidelity worldwide investment

- fidelity international

- fidelity

- skuldkris