Nyhet —

Investera i oroliga tider - en tillbakablick på 2011

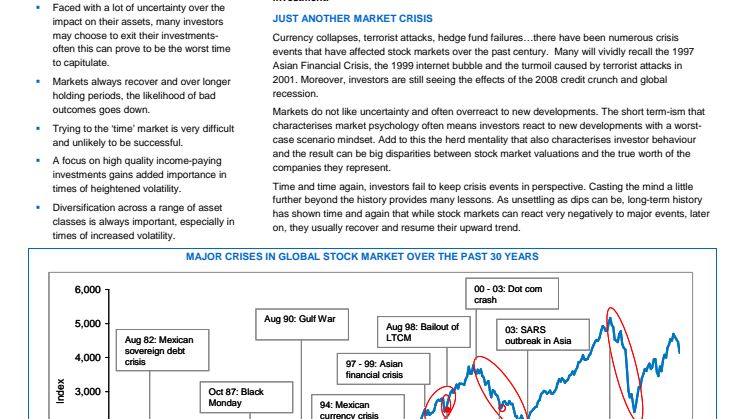

JUST ANOTHER MARKET CRISIS

Currency collapses, terrorist attacks, hedge fund failures…there have been numerous crisis events that have affected stock markets over the past century. Many will vividly recall the 1997 Asian Financial Crisis, the 1999 internet bubble and the turmoil caused by terrorist attacks in 2001. Moreover, investors are still seeing the effects of the 2008 credit crunch and global recession.

Markets do not like uncertainty and often overreact to new developments. The short term-ism that characterises market psychology often means investors react to new developments with a worst-case scenario mindset. Add to this the herd mentality that also characterises investor behaviour and the result can be big disparities between stock market valuations and the true worth of the companies they represent.

Time and time again, investors fail to keep crisis events in perspective. Casting the mind a little further beyond the history provides many lessons. As unsettling as dips can be, long-term history has shown time and again that while stock markets can react very negatively to major events, later on, they usually recover and resume their upward trend.

Perhaps not unsurprisingly, staying invested for the long term is a tune sung by many investment advisors. This advice can be of cold comfort for investors who see the value of their assets decline during crisis periods. However, the validity of this idea should be judged based on the actual historical evidence and in this respect, given the inability of most investors to perfectly time the market, it is remains a very useful maxim.

What other concepts can help investors during periods of heightened market volatility? Fidelity walks you through a few universal investment principles that are as relevant today as they have ever been.

DIVERSIFIED AND DEFENSIVE

A well constructed portfolio should be diversified across asset classes to reduce risks and smooth returns. Defensive assets such as bonds and cash tend to fare better during periods of high market volatility, while growth investments like property and stocks provide attractive returns when economic conditions are expected to be more favourable. The value of bonds and stocks can often move in opposite directions, but taken together, a portfolio that invests in a range of quality assets should deliver attractive returns with lower risk.

Diversification is also important at the security level. During a market crisis, dramatic falls on global stock markets dominate the news headlines and can lead readers to extrapolate negatively about all stocks. However, such thinking is unlikely to be warranted. Certain sectors of the market often perform better than others at different points in the economic cycle.

During a downturn, market conditions tend to favour so-called defensive stocks, as these companies are usually less affected by economic cycles, can maintain earnings and continue paying dividends. Companies like electricity and gas distributors are classic examples. They generally operate under fixed, long term supply contracts and can pass on rising costs directly to the consumers who require energy to power their homes.

On the other hand, the stock prices of growth companies usually outperform as economic conditions improve since their earnings tend to be more sensitive to economic conditions. For example, tourism companies are often among the first to benefit from growing incomes and personal wealth as people have more money to spend on leisure and travel.

This is not to say that all defensive stocks will outperform during downturns; sometimes a traditionally defensive sector may not be favoured due to a range of other factors such as changing industry trends, government policies and competition from other companies. Given that sector return profiles vary according to a broad range of factors, the ability to assess the differential impact of these factors is therefore crucial as is the construction of appropriately well diversified portfolios that help to cancel out company-specific or idiosyncratic risk.

TAKING A LONG TERM VIEW

As we have seen, markets move in cycles. Over short periods, markets can be more volatile and result in a wide range of positive or negative returns. But the longer you stay invested, the greater the probability that your investment will generate a positive return. The graph below from Barclay Capital’s latest Equity Gilt Study shows how over longer holding periods, the probability of negative outcomes narrows progressively. According to Barclay Capital, over the past 85 years, the worst average annualised 20-year return for US equities was 0.9%, while the best was 13.2%. Since this research was conducted on an ex-post basis, it would be incorrect to conclude that it is impossible to lose money by holding equities for 20 year holding period. However, it would be reasonable to say that likelihood of this appears to be very low.

TIME IN THE MARKET, NOT TIMING THE MARKET

It is extremely difficult to predict when is the best time to enter or exit the market. The speed at which markets react to news means stock prices very quickly absorb the impact of new developments. When markets turn, they turn quickly. Those trying to time their entry and exit are therefore likely to miss the bounces. The chart below highlights the impact of an investor in US stocks missing out on the market’s best days over the past 10 years. In 2001 for example, missing out on just the 10 best days in the market would have resulted in negative return for the year as a whole.

CONSIDER THE VALUE OF DIVIDENDS

When things are going well and the stock market is rising strongly, the extra returns from dividends may seem relatively unimportant. However, in weaker markets, the extra return from dividends becomes a valuable part of the total return. Furthermore, the impact of dividends actually becomes amplified over time due to the compounding effect of reinvesting dividends. For example, according to Barclays Capital (Equity Gilt Study 2011), $100 invested in theUSstock market in 1925 would have grown to $9,524 by the end of 2008 without re-investing dividends, but to $302,850 if dividend income was reinvested throughout the period.

Dividends also have the advantage of being more predictable than both corporate earnings because many companies usually strive to maintain their dividends even if their profits are temporarily in decline.

RELYING ON PROFESSIONAL MANAGERS

Professional managers devote considerable time sifting through market information to analyse the true earning potential of every investment. They have a thorough understanding of the market and other issues that could influence a company’s success. To form a well-rounded view, successful investment managers regularly meet with companies, their suppliers, customers and competitors as well as looking at factors such as a company’s competitive position, skills of the management team and general economic conditions to develop a thorough understanding of the investment prospects for each and every stock.

The range of returns across the market can vary significantly from year to year, making good stock selection critical. With around 46,000 stocks listed on exchanges across the world, investing in the expertise of an experienced professional is therefore an important part of successful investing in its own right.

This information is for Investment Professionals only and should not be relied upon by private investors. It must not be reproduced or circulated without prior permission. This communication is not directed at, and must not be acted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. Fidelity/Fidelity Worldwide Investment means FIL Limited and its subsidiary companies. Unless otherwise stated, all views are those of Fidelity. Fidelity only offers information on its own products and services and does not provide investment advice based on individual circumstances. Fidelity, Fidelity Worldwide Investment, the Fidelity Worldwide Investment logo and F symbol are trademarks of FIL Limited. Past performance is not a reliable indicator of future results. Growth Investments Limited is licensed by the MFSA. Fidelity Funds are promoted in Malta by Growth Investments Ltd in terms of the EU UCITS Directive and Legal Notices 207 and 309 of 2004. The Funds are regulated in Luxembourg by the Commission de Surveillance du Secteur Financier; Our legal representative in Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich. Paying agent for Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich.Issued by FIL Investments International (FSA registered number 122170) a firm authorised and regulated by the Financial Services Authority. FIL Investments International is a member of the Fidelity Worldwide Investment group of companies and is registered in England and Wales under the company number 1448245. The registered office of the company is Oakhill House, 130 Tonbridge Road, Hildenborough, Tonbridge, Kent TN11 9DZ, United Kingdom. Fidelity Worldwide Investment’s VAT identification number is 395 3090 35. SSO4785/1212

Ämnen

- Finans

Kategorier

- fidelity

- fidelity international

- fidelity worldwide investment

- finanskrisen

- market volatility

- återhämtning

- investera