Nyhet -

Is "core" Europe stalling?

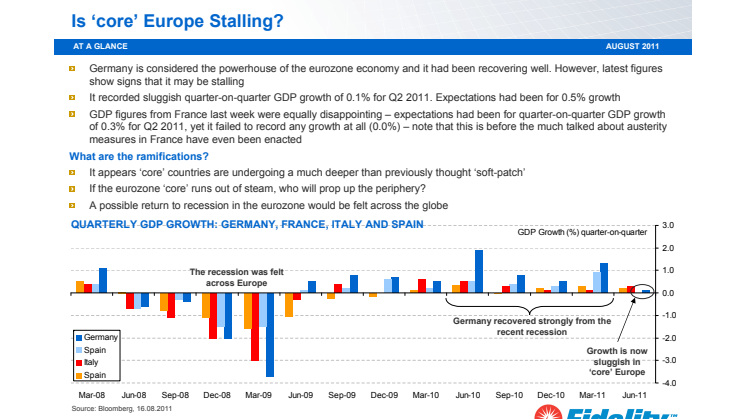

- Germany is considered the powerhouse of the eurozone economy and it had been recovering well. However, latest figures show signs that it may be stalling

- It recorded sluggish quarter-on-quarter GDP growth of 0.1% for Q2 2011. Expectations had been for 0.5% growth

- GDP figures from France last week were equally disappointing – expectations had been for quarter-on-quarter GDP growth of 0.3% for Q2 2011, yet it failed to record any growth at all (0.0%) – note that this is before the much talked about austerity measures in France have even been enacted

What are the ramifications?

- It appears ‘core’ countries are undergoing a much deeper than previously thought ‘soft-patch’

- If the eurozone ‘core’ runs out of steam, who will prop up the periphery?

- A possible return to recession in the eurozone would be felt across the globe

Will the ECB need to reverse course?

Generally, data for Germany and France has been soft across the board – manufacturing, which initially rebounded strongly after the recession, has waned in recent months. These extremely soft data make the ECB’s two recent interest rate hikes seem ill-timed – there is a debate over whether they should reverse course – to do so would cause the ECB a great deal of embarrassment. Although it was also forced to do a U-turn in 2008.

But it is not all doom and gloom…

Current valuations on European equities have already priced in a significant slowdown in economic growth (possibly recession) to such an extent that there are many good quality names that might represent excellent value. Even in a slow growth environment, companies that are market leaders in their field, which have maintained strong balance sheets and delivered strong returns on capital are likely to outperform their peers.

Some thoughts from our fund managers...

“Stepping aside from the short term market, volatility there are structural trends which will support global growth and continue to provide individual opportunities. In pursuing these opportunities, I see the German companies well placed given healthy balance sheets and their strong competitiveness as evidenced by unit labour costs, brand strength and innovation. In fact I am finding many high-quality companies with decent growth opportunities and attractive sustainable dividend yields above 4.0%, which makes me cautiously optimistic.”

Christian von Engelbrechten, German equities, Fidelity International

“There is a lot of uncertainty as to the future course of events but this is to a large extent getting reflected in stock prices. On long-term trend earnings, the European market is trading on 10x earnings, which is cheap relative to history. The only other period in recent times that the market was this cheap was back in the early 1980s when bond yields globally were significantly higher."

Parus Shah, European equities, Fidelity International

Ämnen

- Finans

Kategorier

- france

- germany

- återhämtning

- market volatility

- investeringar

- investera

- finanskrisen

- fidelity international

- fidelity

- ecb