Nyhet -

Keeping the eurozone in context

- Despite the current gloom, investors should be wary of allowing well-documented problems in the eurozone to cloud their views of global equity markets. A number of considerations support a more balanced view towards global equities.

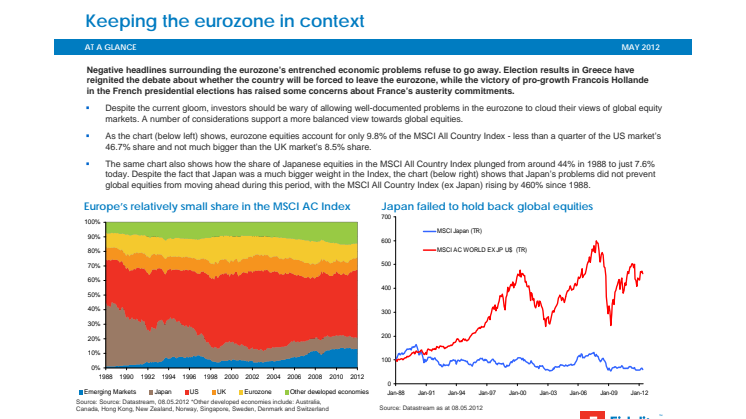

- As the chart in the attached document shows, eurozone equities account for only 9.8% of the MSCI All Country Index - less than a quarter of the US market’s 46.7% share and not much bigger than the UK market’s 8.5% share.

- The same chart also shows how the share of Japanese equities in the MSCI All Country Index plunged from around 44% in 1988 to just 7.6% today. Despite the fact that Japan was a much bigger weight in the Index, the chart (below right) shows that Japan’s problems did not prevent global equities from moving ahead during this period, with the MSCI All Country Index (ex Japan) rising by 460% since 1988.

The bigger picture

Some other factors to consider:

Intra-eurozone differences: even within the eurozone, the story is not universally bad. The German economy and many German companies have actually performed remarkably well throughout the crisis period. Moreover, many of the most problematic countries are economically insignificant in terms of size. For example, Greece accounts for only 2% of eurozone GDP1 and less than 0.5% of global GDP2.

The global view: the eurozone accounted for only 14% of global GDP in 20113; its problems shouldn’t prevent the broader global economy from growing at respectable pace (last month, the IMF actually raised its 2012 global growth forecast to 3.5% from 3.3% previously). This reflects the fact that many parts of the global economy are performing well, including the US economy and many emerging markets.

Contained commodity prices: Just as was the case with Japan back in the 80s and 90s, it can be argued that the economic weakness in the eurozone can keep a lid on global commodity prices, which allows the rest of the world to grow more strongly for a sustained period.

The importance of good asset allocation: large global and intra-eurozone economic differences underscore the importance of good asset allocation. Investors that overweighted US equities and underweighted the eurozone’s problem countries would have enjoyed good returns. For example, US equities are up by my more than 8% since the start of the year.

Sources:1 Financial Times; 2 Economist Intelligence Unit; 3 IMF (2011 GDP adjusted for purchasing power).

“Japan’s problems didn’t stop the rest of the world’s stock markets making good progress. In fact, it can be argued that a weak Japan dampened commodity price inflation and allowed the rest of the world to grow a little faster than otherwise would have been possible. While Europe has problems, investors should not forget that there is growth elsewhere in the world and multi-asset funds can tilt allocations regionally within their equity exposure.”

Trevor Greetham, Multi Asset funds

This information is for Investment Professionals only and should not be relied upon by private investors. It must not be reproduced or circulated without prior permission. This communication is not directed at, and must not be acted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. Fidelity/Fidelity Worldwide Investment means FIL Limited and its subsidiary companies. Unless otherwise stated, all views are those of Fidelity. Fidelity only offers information on its own products and services and does not provide investment advice based on individual circumstances. Fidelity, Fidelity Worldwide Investment, the Fidelity Worldwide Investment logo and F symbol are trademarks of FIL Limited. Past performance is not a reliable indicator of future results. Growth Investments Limited is licensed by the MFSA. Fidelity Funds are promoted in Malta by Growth Investments Ltd in terms of the EU UCITS Directive and Legal Notices 207 and 309 of 2004. The Funds are regulated in Luxembourg by the Commission de Surveillance du Secteur Financier; Our legal representative in Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich. Paying agent for Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich.Issued by FIL Investments International (FSA registered number 122170) a firm authorised and regulated by the Financial Services Authority. FIL Investments International is a member of the Fidelity Worldwide Investment group of companies and is registered in England and Wales under the company number 1448245. The registered office of the company is Oakhill House, 130 Tonbridge Road, Hildenborough, Tonbridge, Kent TN11 9DZ, United Kingdom. Fidelity Worldwide Investment’s VAT identification number is 395 3090 35.. SSO5237/0513

Ämnen

- Finans

Kategorier

- fidelity

- fidelity international

- fidelity worldwide investment

- eurozone

- election

- greece

- trevor greetham