Nyhet -

QE3 – Fed attempts to boost the real economy

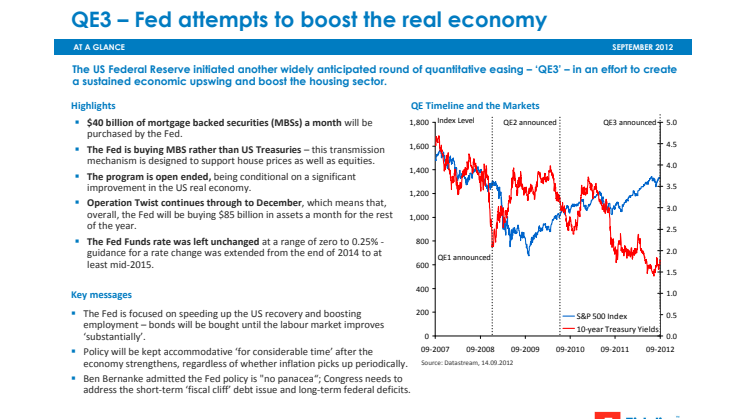

The US Federal Reserve initiated another widely anticipated round of quantitative easing – ‘QE3’ – in an effort to create a sustained economic upswing and boost the housing sector.

Highlights:

- $40 billion of mortgage backed securities (MBSs) a month will be purchased by the Fed.

- The Fed is buying MBS rather than US Treasuries – this transmission mechanism is designed to support house prices as well as equities.

- The program is open ended, being conditional on a significant improvement in the US real economy.

- Operation Twist continues through to December, which means that, overall, the Fed will be buying $85 billion in assets a month for the rest of the year.

- The Fed Funds rate was left unchanged at a range of zero to 0.25% - guidance for a rate change was extended from the end of 2014 to at least mid-2015.

Key messages:

- The Fed is focused on speeding up the US recovery and boosting employment – bonds will be bought until the labour market improves ‘substantially’.

- Policy will be kept accommodative ‘for considerable time’ after the economy strengthens, regardless of whether inflation picks up periodically.

- Ben Bernanke admitted the Fed policy is "no panacea“; Congress needs to address the short-term ‘fiscal cliff’ debt issue and long-term federal deficits.

Implications of QE3

Q3 is a little different; for the first time the Fed has explicitly tied policy to improvements in the real economy

The implications:

- Mortgage bonds will benefit from QE3 – the aim is to boost the housing market and, in turn, support the real economy.

- The Fed is likely to own more than 50% of current coupon mortgage issuance in seven to eight months’ time at the rate of purchase laid out. There is a risk of some market dislocation as supply of MBSs becomes scarce.

- As the Fed removes mortgage bonds from the market, investors in search of yield will be forced into traditionally higher risk assets.

- Higher-yielding equity and real estate markets are likely to be beneficiaries of this search for yield, as well as improved sentiment and liquidity.

The market reaction:

- Stock markets reacted positively to the news, with economically sensitive sectors and stocks making gains.

- Commodities have also rallied on hopes of a pick-up in the global economy. §Yields on Fannie Mae-guaranteed mortgage bonds fell, highlighting the programme’s potential to boost the housing sector.

- The lack of additional Treasury buying weighed at the long end of the treasury yield curve.

Views from our investment teams

“Once again the US Federal Reserve has upstaged the European Central Bank (ECB) with a powerful and open-ended easing program aimed right at the core of the problem - housing finance. Ben Bernanke is the world expert on what the Fed should have done to get out of the Great Depression and he is following the playbook to the line - ease aggressively, don't reverse course and keep the easing going well into the recovery. The Fed's actions support our long-standing overweight of US equities versus Europe and global property in multi-asset funds. As for markets, we may see a period of consolidation as those who bought the well-flagged rumour sell the news. We're hopeful this easing will help trigger a new economic upswing but these things don't happen overnight. Soft economic data could create some good buying opportunities in the next few months.”

Trevor Greetham, Multi Asset Funds

“The much awaited latest round of monetary stimulus, QE3, complements the bold moves of the ECB the previous week. In combination, the ECB’s commitment to buy ‘unlimited’ amounts of Euro sovereign bonds, combined with the Fed’s program to buy mortgage backed securities (MBS) and keep interest rates low for many years, is perceived to provide a much needed boost at a time when global growth is anaemic and deteriorating. The Fed is targeting the MBS market in order to kick-start the housing market, which is the area of the economy to show least improvement since the 2009 recovery. They hope to drive mortgage interest rates lower, and thus spur demand for homes which would improve consumer confidence and provide jobs. Financial and commodity assets responded immediately to the announcement even though it was expected. Whilst a further boost may help short term sentiment and reverse the economy’s deceleration it does not address the long term structural issues of fiscal imbalances and government indebtedness and therefore with the US market already at a post recession high and valuations just fair the impact on the market may be short-lived.”

Adrian Brass, US Equities

This information is for Investment Professionals only and should not be relied upon by private investors. It must not be reproduced or circulated without prior permission. This communication is not directed at, and must not be acted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. Research professionals include associates, analysts, country and sector managers who retain research responsibility and technical & quantitative analysts who are part of the research groups. Fidelity/Fidelity Worldwide Investment means FIL Limited and its subsidiary companies. Unless otherwise stated, all views are those of Fidelity. Fidelity only offers information on its own products and services and does not provide investment advice based on individual circumstances. Fidelity, Fidelity Worldwide Investment, the Fidelity Worldwide Investment logo and F symbol are trademarks of FIL Limited. No statements or representations made in this document are legally binding on Fidelity or the recipient. Any proposal is subject to contract terms being agreed. Growth Investments Limited is licensed by the MFSA. Fidelity Funds are promoted in Malta by Growth Investments Ltd in terms of the EU UCITS Directive and Legal Notices 207 and 309 of 2004. The Funds are regulated in Luxembourg by the Commission de Surveillance du Secteur Financier; Our legal representative in Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich. Paying agent for Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich.Issued by FIL Investments International (FSA registered number 122170) a firm authorised and regulated by the Financial Services Authority. FIL Investments International is a member of the Fidelity Worldwide Investment group of companies and is registered in England and Wales under the company number 1448245. The registered office of the company is Oakhill House, 130 Tonbridge Road, Hildenborough, Tonbridge, Kent TN11 9DZ, United Kingdom. Fidelity Worldwide Investment’s VAT identification number is 395 3090 35. IC12/59

Ämnen

- Finans

Kategorier

- trevor greetham

- fed

- fidelity worldwide investment

- fidelity international

- fidelity