Nyhet -

Trevor Greetham´s Investment Clock July 2012: The "M" shaped cycle

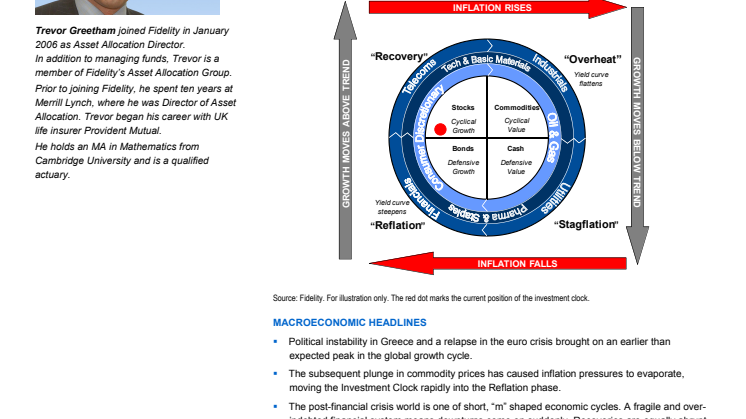

THE INVESTMENT CLOCK

The Investment Clock approach generates growth and inflation readings based on past trends and the current momentum of lead indicators. These indicators are updated on a monthly basis to build an expectation of how the global economy may perform over the coming three to six months.

The growth reading sets the relative weighting of cyclical and defensive assets (North-South axis). The inflation reading sets the weighting of financial assets versus real assets (East-West axis).

MACROECONOMIC HEADLINES

- Political instability in Greece and a relapse in the euro crisis brought on an earlier than expected peak in the global growth cycle.

- The subsequent plunge in commodity prices has caused inflation pressures to evaporate, moving the Investment Clock rapidly into the Reflation phase.

- The post-financial crisis world is one of short, “m” shaped economic cycles. A fragile and over-indebted financial system means downturns come on suddenly. Recoveries are equally abrupt as policy makers respond to market stress, but they fade as soon as stimulus ends.

ASSET ALLOCATION HEADLINES

- Diversification across asset classes is more important than ever and strategic benchmarks should include safe haven or uncorrelated investments, like high quality sovereign bonds and gold.

- We moved bonds overweight during the month of May by reducing our exposure to stocks and commodities.

- However, we remain positive on global property. Credit conditions for US property loans are easing.

- Within equities, we continue to overweight US equities at the expense of European equities.

GLOBAL GROWTH

Our global growth scorecard is weakening on the back of falls in business confidence, economist GDP downgrades and a rolling over of the OECD’s lead indicators.

INFLATION

The inflation scorecard has moved sharply negative in line with the collapse in oil prices. This means that combined with our weakening global growth scorecard, the Investment Clock model is moving into bond-friendly Reflation. The absence of inflation risks should clear the way for a wide range of central banks to ease policy.

However, we are concerned investors may be too optimistic on the degree of ease that will come in the near term, particularly in the US where economic data is only just starting to weaken. High thresholds to action by policy makers suggest things may have to get worse before they get better and it could still take several months before the conditions for a new recovery are in place.

SHORT CYCLES, HIGH THRESHOLDS

The post-financial crisis period is one of short “m” shaped cycles. The four mini-cycles since 2007 have seen upswings averaging only six months and downswings only nine months. Recoveries have been driven by policy ease, fading as soon as stimulus ends.

High thresholds to action exacerbate both the intensity of downturns and the abruptness of recoveries. In Europe, political leaders are faced with opposition both to austerity and to bail outs.

The June summit was positive as euro level capital injections into banks should weaken the negative feedback loop for peripheral sovereigns. However, political risks remain high with the link between austerity, unemployment and asset price declines intact. Stress is likely to intensify again unless global growth picks up.

Markets have high hopes of quantitative ease from the Fed but we see high thresholds to action here too. Unconventional ease comes in large multi-month programs, not easily reversed.

With stock prices near cycle highs, the Fed will want to keep its powder dry. In recent years, we’ve needed to see long term inflation expectations break to the downside and equity market volatility spike before they have eased with any force.

THE INVESTMENT CLOCK

The growth and inflation readings feed into the Investment Clock model to determine a probability for each of the four cycles of the Clock prevailing in the coming three to six month period. By plotting indicators for growth and inflation against each other in two dimensions, we monitor the economic cycle as it evolves. The recent plunge in commodity prices has caused inflation pressures to evaporate, moving the Investment Clock rapidly into the Reflation phase.

For more information and charts, please see attached PDF document.

Trevor Greetham joined Fidelity in January 2006 as Asset Allocation Director.

In addition to managing funds, Trevor is a member of Fidelity’s Asset Allocation Group.

Prior to joining Fidelity, he spent ten years at Merrill Lynch, where he was Director of Asset Allocation. Trevor began his career with UK life insurer Provident Mutual. He holds an MA in Mathematics from Cambridge University and is a qualified actuary.

This document is for investment professionals only and should not be relied upon by private investors. It must not be reproduced or circulated without prior permission. This communication is not directed at, and must not be acted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. Fidelity/ Fidelity International means FIL Limited, and its subsidiary companies. Unless otherwise stated, all views are those of the Fidelity organisation. Investors should note that the views expressed may no longer be current and may have already been acted upon by Fidelity. The research and analysis used in this material is gathered by Fidelity for its use as an Investment Manager and may have already been acted upon for its own purposes. Reference in this document to specific securities should not be construed as a recommendation to buy or sell these securities, but is included for the purposes of illustration only. Fidelity only offers information on its own products and services and does not provide investment advice based on individual circumstances. Fidelity, Fidelity Worldwide Investment and the Fidelity Worldwide Investment and F symbol are trademarks of FIL Limited. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up and investors may not get back the amount invested. Fidelity’s legal representative in Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich. Paying agent for Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich. Malta: Growth Investments Limited is licensed by the MFSA. Fidelity Funds is promoted in Malta by Growth Investments Ltd in terms of the EU UCITS Directive and Legal Notices 207 ad 309 of 2004. The Fund is regulated in Luxembourg by the Commission de Surveillance du Secteur Financier. Issued by FIL Investments International (registered in England and Wales), authorised and regulated in the UK by the Financial Services Authority. IC12/18

Ämnen

- Finans

Kategorier

- fidelity

- fidelity international

- fidelity worldwide investment

- trevor greetham

- investment clock