Nyhet -

Trevor Greetham's Investment Clock March: Prefer stocks to commodities

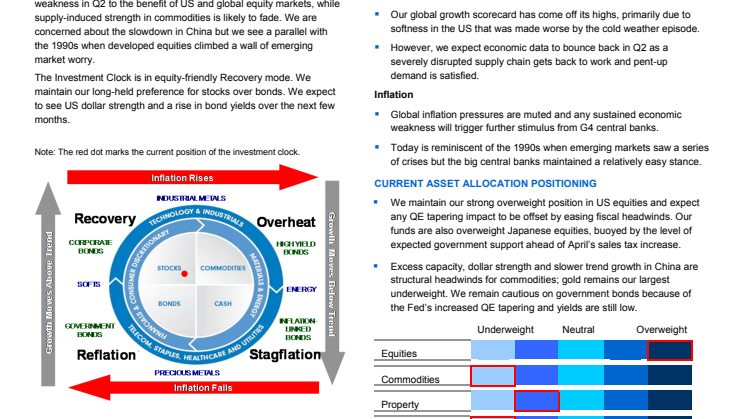

Commodities have outperformed stocks since the start of the year. We expect the US economy to bounce back from weather-induced weakness in Q2 to the benefit of US and global equity markets, while supply-induced strength in commodities is likely to fade. We are concerned about the slowdown in China but we see a parallel with the 1990s when developed equities climbed a wall of emerging market worry.

The Investment Clock is in equity-friendly Recovery mode. We maintain our long-held preference for stocks over bonds. We expect to see US dollar strength and a rise in bond yields over the next few months.

LEAD INDICATORS IN FOCUS

Growth

- Our global growth scorecard has come off its highs, primarily due to softness in the US that was made worse by the cold weather episode.

- However, we expect economic data to bounce back in Q2 as a severely disrupted supply chain gets back to work and pent-up demand is satisfied.

Inflation

- Global inflation pressures are muted and any sustained economic weakness will trigger further stimulus from G4 central banks.

-Today is reminiscent of the 1990s when emerging markets saw a series of crises but the big central banks maintained a relatively easy stance.

CURRENT ASSET ALLOCATION POSITIONING

- We maintain our strong overweight position in US equities and expect any QE tapering impact to be offset by easing fiscal headwinds. Our funds are also overweight Japanese equities, buoyed by the level of expected government support ahead of April’s sales tax increase.

- Excess capacity, dollar strength and slower trend growth in China are structural headwinds for commodities; gold remains our largest underweight. We remain cautious on government bonds because of the Fed’s increased QE tapering and yields are still low.

Ämnen

- Finans