Nyhet —

Trevor Greetham's Investment Clock May: A Summer Lull

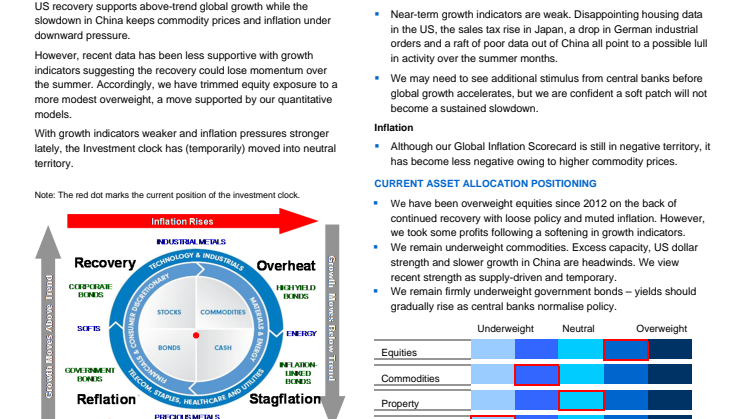

We expect the Investment Clock to spend most of its time in equity-friendly Recovery mode over the next few years as the US recovery supports above-trend global growth while the slowdown in China keeps commodity prices and inflation under downward pressure.

However, recent data has been less supportive with growth indicators suggesting the recovery could lose momentum over the summer. Accordingly, we have trimmed equity exposure to a more modest overweight, a move supported by our quantitative models.

With growth indicators weaker and inflation pressures stronger lately, the Investment clock has

(temporarily) moved into neutral territory.

LEAD INDICATORS IN FOCUS

Growth

-Near-term growth indicators are weak. Disappointing housing data in the US, the sales tax rise in Japan, a drop in German industrial orders and a raft of poor data out of China all point to a possible lull in activity over the summer months.

-We may need to see additional stimulus from central banks before global growth accelerates, but we are confident a soft patch will not become a sustained slowdown.

Inflation

-Although our Global Inflation Scorecard is still in negative territory, it has become less negative owing to higher commodity prices.

CURRENT ASSET ALLOCATION POSITIONING

-We have been overweight equities since 2012 on the back of continued recovery with loose policy and muted inflation. However, we took some profits following a softening in growth indicators.

-We remain underweight commodities. Excess capacity, US dollar strength and slower growth in China are headwinds. We view recent strength as supply-driven and temporary.

-We remain firmly underweight government bonds – yields should gradually rise as central banks normalise policy.

Ämnen

- Finans