Press release -

Results for the fourth quarter and year to 31 March 2016

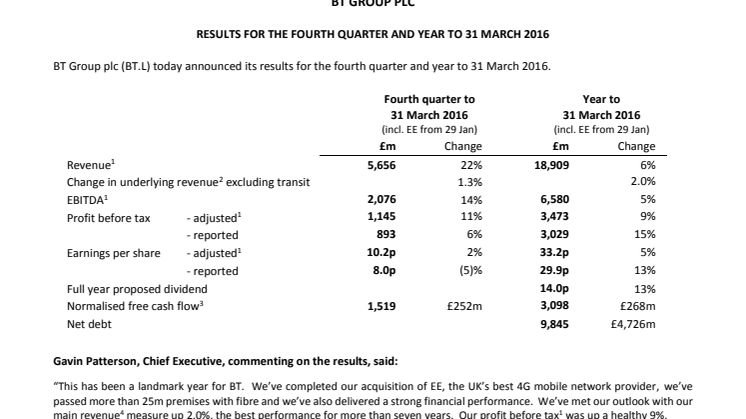

BT Group plc (BT.L) today announced its results for the fourth quarter and year to 31 March 2016.

Gavin Patterson, Chief Executive, commenting on the results, said:

“This has been a landmark year for BT. We’ve completed our acquisition of EE, the UK’s best 4G mobile network provider, we’ve passed more than 25m premises with fibre and we’ve also delivered a strong financial performance. We’ve met our outlook with our main revenue4 measure up 2.0%, the best performance for more than seven years. Our profit before tax1 was up a healthy 9%.

“Customers want to be online wherever they are and we will be there for them. Our multi-billion pound investment plans will see both fibre and 4G reach 95% of the UK and we won't stop there. The UK is a digital leader and our investment in ultrafast broadband will help it stay ahead.

“The integration of EE is going well and we now see the opportunity to deliver more synergies than we originally expected, and at a lower cost. And we’re reorganising our business to better serve customers both in the UK and internationally.

“We’ve invested across the business and are seeing good results. Our BT Sport audiences are up 45 per cent this year following the launch of UEFA Champions League and UEFA Europa League content. BT Mobile has done well since its launch, building a customer base of over 400,000. And in the business market, we’ve seen very strong demand for our cyber security expertise with our security business growing by 24%.

“Customers are benefiting from our investments but we plan to do more when it comes to service, to meet customers’ rising expectations. That’s why Openreach is tackling missed appointments, why BT Consumer will be upgrading service levels to next day repair and why we’ve hired 900 engineers. We’ve also recruited more than 900 extra contact centre staff. This will enable us to return EE and BT Consumer contact centre work to the UK.

“Our strong overall performance for the year is reflected in our full year dividend, which is up 13%. Our results and the investments we’re making position us well to continue to grow in the coming years. In light of our confidence we are setting out financial and dividend guidance for the next two years.”

1 Before specific items. Includes EE from 29 January 2016

2 Excludes specific items, foreign exchange movements and the effect of acquisitions and disposals

3 Before specific items, pension deficit payments and the cash tax benefit of pension deficit payments

4 Change in underlying revenue excluding transit

Key points for the fourth quarter:

- Our acquisition of EE completed on 29 January 2016

- Underlying revenue1 excluding transit up 1.3%

- Underlying operating costs2 excluding transit up 2% primarily reflecting our investment in BT Sport Europe

- EBITDA3 up 14% including £261m from EE

- Openreach achieved 415,000 fibre broadband net additions with other service providers connecting 48% of these

- Combined BT and EE broadband4 net additions market share of 81%

Key points for the year:

- Underlying revenue1 excluding transit up 2.0%, our best performance for more than seven years

- EBITDA3 of £6,580m, up 5%, including £261m from EE

- Earnings per share3 up 5%

- Normalised free cash flow5 of £3,098m, up 9%, including £261m impact from EE

- Proposed final dividend of 9.6p, up 13%, giving a full year dividend of 14.0p, also up 13%

- BT Consumer TV customer base grew by 28% to 1.5m

- Fibre broadband available to more than 25m premises

Performance against 2015/16 outlook:

In February we reaffirmed our EBITDA and free cash flow outlook and clarified that we expected underlying revenue excluding transit to grow by 1% to 2%. This outlook excluded the impact of acquiring EE and we have set out below how we performed on this basis.

Outlook:

Our outlook for 2016/17 and 2017/18 is as follows:

Our 2016/17 outlook assumes a net investment of around £100m against EBITDA and normalised free cash flow from launching handset offerings to BT Mobile customers.

Also included in the above normalised free cash flow outlook, we expect around £100m of EE integration capital expenditure in each of 2016/17 and 2017/18. We also expect capital expenditure of up to £300m in 2016/17 and around £100m in 2017/18 relating to the Emergency Services Network contract won by EE in December 2015.

1 Excludes specific items, foreign exchange movements and the effect of acquisitions and disposals

2 Excludes specific items, foreign exchange movements and the effect of acquisitions and disposals and is before depreciation and amortisation

3 Before specific items

4 DSL and fibre

5 Before specific items, pension deficit payments and the cash tax benefit of pension deficit payments

6 Excludes the impact of EE

7 Measured as though EE had been part of the group from 1 April 2015, see page 4

GROUP RESULTS FOR THE FOURTH QUARTER AND YEAR TO 31 MARCH 2016

Line of business results2

1 Includes EE from 29 January 2016

2 Before specific items. Specific items are defined in Note 4 to the condensed consolidated financial statements

3 Excludes specific items, foreign exchange movements and the effect of acquisitions and disposals

4 Before specific items, pension deficit payments and the cash tax benefit of pension deficit payments. Line of business operating cash flows exclude interest, tax and integration capital expenditure which are classified within Other

n/m = not meaningful

Notes:

1. Our commentary focuses on the trading results on an adjusted basis, which is a non-GAAP measure, being before specific items. Unless otherwise stated, revenue, operating costs, earnings before interest, tax, depreciation and amortisation (EBITDA), operating profit, profit before tax, net finance expense, earnings per share (EPS) and normalised free cash flow are measured before specific items. This is consistent with the way that financial performance is measured by management and reported to the Board and the Operating Committee and assists in providing a meaningful analysis of the trading results of the group. The directors believe that presentation of the group’s results in this way is relevant to the understanding of the group’s financial performance as specific items are those that in management’s judgement need to be disclosed by virtue of their size, nature or incidence. In determining whether an event or transaction is specific, management considers quantitative as well as qualitative factors such as the frequency or predictability of occurrence. Specific items may not be comparable with similarly titled measures used by other companies. Reported revenue, reported operating costs, reported EBITDA, reported operating profit, reported profit before tax, reported net finance expense, reported EPS and reported free cash flow are the equivalent unadjusted or statutory measures. Reconciliations of reported to adjusted revenue, operating costs and operating profit are set out in the Group income statement. Specific items are set out in Note 4. Reconciliations of EBITDA, adjusted profit before tax and adjusted EPS to the nearest measures prepared in accordance with IFRS are provided in Notes 8, 9 and 10 respectively.

2. Trends in underlying revenue, trends in underlying operating costs, and underlying EBITDA are non-GAAP measures which seek to reflect the underlying performance of the group that will contribute to long-term sustainable growth and as such exclude the impact of acquisitions and disposals, foreign exchange movements and any specific items. We focus on the trends in underlying revenue and underlying operating costs excluding transit as transit traffic is low-margin and is affected by reductions in mobile termination rates. Given the significance of the EE acquisition to the group, in 2016/17 we will calculate underlying revenue excluding transit as though EE had been part of the group from 1 April 2015. This is different from how we usually adjust for acquisitions, and is the basis for our 2016/17 outlook.

BT GROUP PLC RESULTS FOR THE YEAR TO 31 MARCH 2016

OVERVIEW

Invest for growth

This has been a landmark year for BT. We acquired EE on 29 January, bringing together the UK’s best 4G mobile network and the largest superfast fixed network. This makes us the UK’s leading converged communications provider. The acquisition supports our strategy of investing for growth, and gives us a great platform to build upon. We want to transform the shape of communications by creating converged products and services to meet the growing demand from UK consumers and businesses.

The investments we’ve been making have driven our strong financial performance for the year. Our key revenue measure of underlying revenue excluding transit (which excludes EE) was up 2.0%, at the top end of our outlook range of 1% to 2%. And it’s our best growth in more than seven years.

This performance was mainly driven by BT Consumer where revenue was up 7% reflecting 17% growth in broadband and TV revenue, helped by our investments in BT Sport Europe and BT Mobile. Openreach revenue was up 2% with fibre broadband growth offsetting regulatory headwinds.

Underlying revenue excluding transit was up 1% in BT Wholesale and down 2% in BT Global Services whilst BT Business remained flat. We’re investing in our products, network and expertise to increase our share of spending by business customers. We’ve improved our product portfolio to meet their needs as they increasingly adopt IP and cloud-based services. This year we also launched a number of cyber security products, including BT Assure Cyber Defence, an advanced security platform for monitoring, detecting and protecting against cyber-threats.

Transform our costs

Our cost transformation approach is based on a methodology honed over a decade and underpinned by forensic data analysis, strong governance and the support of senior management. We’ve achieved further savings in the year, helped by major end-to-end programmes across multiple lines of business. We’re confident there is plenty more we can do and we see the opportunity to take well over £1bn out of our gross costs over the next two years.

Underlying operating costs1 excluding transit were up 2%. As previously highlighted, we’re no longer benefiting from the sale of redundant copper and our costs have been impacted by higher leaver charges (as last year most were included within specific items), a higher pensions operating charge and our investment in BT Sport Europe. Without these effects, underlying operating costs1 excluding transit would have been down 2%.

Excluding EE, adjusted EBITDA for BT was up 1%, in line with our outlook, with our revenue growth and cost transformation activities more than offsetting the negative cost impacts above. This EBITDA performance contributed to normalised free cash flow of £2,837m excluding EE, again in line with our outlook.

Deliver superior customer service

We’ve made progress on service in a number of areas this year. Openreach achieved all 60 of the minimum service levels set by Ofcom and, in BT Consumer, complaints are 50% lower where our agents have been multi-skilled. We’ve also launched a number of tools that give customers greater control over their orders, bills and services. Our new MyBT app, for example, has been downloaded by more than 400,000 people so far, as customers increasingly want to use digital channels for service. View My Engineer also allows customers to track engineer appointments. But in some areas we didn’t do as well as we’d intended. For example, it took us longer than it should have to deliver some services, particularly Ethernet products.

Our performance in the first quarter of the year was strong with good service levels. But in the second, third and fourth quarters, our service was significantly impacted by summer electrical storms, system and network outages and winter storms. We recovered well in the fourth quarter and ended the year on a positive trajectory. But this wasn’t enough to improve our ‘Right First Time’ measure which was down 3.0% (2014/15: up 4.7%).

As connectivity becomes ever more critical to how we live and work, our customers have rising expectations of the service we provide. Quality of service is becoming more important than price alone. While we did make improvements in the year, we’re not where we want to be. That’s why we’ve hired more than 900 extra contact centre staff and 900 new engineers, why Openreach is tackling missed appointments, why BT Consumer will be upgrading service levels to next day repair, Monday to Saturday, and why both EE and BT Consumer are returning contact centre work to the UK.

1 Excludes specific items, foreign exchange movements and the effect of acquisitions and disposals and is before depreciation and amortisation

Mobility

We acquired EE on 29 January 2016. The purchase consideration comprised 1,595m BT shares valued at £7.5bn and cash of £3.5bn, of which £3.2bn was funded through our committed acquisition facility. After a provisional fair value exercise, we’ve allocated this consideration between goodwill of £6.5bn and net assets acquired of £4.5bn (see Note 6).

EE has a customer base of 30.6m and we’re pleased with its financial performance since we took ownership. BT Mobile has also done well in the year since its launch, building a customer base of over 400,000.

We’re making good progress on integrating EE and have identified further synergy opportunities. We now expect cost synergies to reach a run-rate of around £400m per year in the fourth full year (previously around £360m) of which we expect to realise £100m in 2016/17. We also expect the cost of integrating EE to be lower than previously planned, at around £550m. The capital expenditure part of this, including around £100m in both 2016/17 and 2017/18, will not be treated as a specific item and therefore will be reflected in our normalised free cash flow in these years.

Broadband

With Openreach being part of the wider group, we’ve had the confidence and ability to invest at scale and pace in the UK’s digital infrastructure. So far we’ve passed more than 25m premises with our fibre broadband network, around 85% of the UK. In total, this means 90% of the UK can now get fibre broadband speeds from all networks and we’re on track to help bring fibre to 95% of the country by the end of 2017, with plans to go even further.

G.fast technology is now being trialled in three locations, offering speeds of up to 330Mbps and we have a further two trials planned for 2016/17. Openreach will also be conducting two trials of business Fibre-to-the-Premises (FTTP) in Bradford, providing ultrafast speeds of up to 1Gbps. Our lab trials (conducted together with Bell Labs) of XG-FAST technology have achieved speeds of more than 5Gbps. We have a wide range of technologies that we will use to help the UK maintain its position as a leading digital economy.

Openreach achieved 415,000 fibre broadband net additions in the fourth quarter, a decrease of 9% against a strong performance in the previous year. Other service providers connected 48% of these, demonstrating consistent market-wide demand for fibre. We have now connected around 5.9m homes and businesses, 23% of those passed and more than 40% higher than a year ago. Including EE, we added 214,000 retail fibre broadband customers in the quarter, taking our own fibre broadband customer base to 4.1m. This means almost half of our retail broadband customers are now on fibre. The UK broadband market1 grew by 130,000 in the fourth quarter, of which our retail share was 105,000 or 81%.

TV

BT Consumer now has 1.5m TV customers, an increase of 28% since the start of the year. We’ve expanded our TV offerings, stimulating more demand for our channels. In July 2015, we launched Europe’s very first live sports Ultra HD (4K) channel, BT Sport Ultra HD. We later added Netflix Ultra HD. BT Sport’s average daily audience figures increased 45% year on year, from the start of the football season in August to the end of March. For the same period, we saw 39 match events with peak concurrent viewers of over 1m. And the UEFA Europa League last 16 first leg clash between Liverpool and Manchester United generated a peak of more than 2m viewers for the first time.

Transforming our organisation

Our integration of EE into the wider group is well underway, and that has provided the opportunity to reorganise our business to better serve our different types of customers. We’ve reported our results to 31 March 2016 under six customer-facing lines of business: BT Global Services, BT Business, BT Consumer, EE, BT Wholesale and Openreach. With effect from 1 April 2016, the customer-facing lines of business are now: Global Services, Business and Public Sector, Consumer, EE, Wholesale and Ventures, and Openreach. We will report under this new structure in our first quarter results for 2016/17.

We want to be the leading converged services provider in the UK and the combination of BT's leading fibre network with EE's leading mobile network puts us in a very strong position as the UK market continues its digital transformation. We believe we can offer the products and services that customers want, supported by the best UK networks. This should allow us to grow the number of products and services that we sell. Consumer is targeting a 2.5m increase in its Revenue Generating Units over the next three years.

For business customers, we want to grow our share of their spend, by increasing the number of products and services we sell them. In particular, we see opportunities to exploit our expertise in protecting organisations against cyber-threats, and to sell more IP and cloud-based products, leveraging our Cloud of Clouds strategy. Global Services is aiming to increase its share of spend by its Global Accounts by 10% over the next three years. And Business and Public Sector has the ambition of increasing its Revenue Generating Units by 15% over the same period.

1 DSL and fibre

We announced in March that our Group Finance Director, Tony Chanmugam, has decided to leave BT after many successful years with the company. He will be replaced by Simon Lowth, who will join in July having served as CFO for a number of major international companies. Following a handover, Tony’s focus for a period of time will be on integrating EE into BT.

Income statement

Reported revenue was £19,042m, up 6%. Adjusted revenue, which is before specific items, was £18,909m, also up 6%. EE contributed £1,038m of external revenue in the two months since we acquired it. We had a £127m negative impact from foreign exchange movements, a £109m reduction in transit revenue and a £6m negative impact from disposals. Excluding these, underlying revenue excluding transit was up 2% which is at the top end of our outlook range of growth of 1% to 2%.

Adjusted operating costs1 increased £749m to £12,329m. Of this £725m relates to EE with a large proportion within Other costs. These were up £406m or 12% for the group, primarily reflecting EE’s subscriber acquisition and retention costs, offset by favourable foreign exchange movements. Programme rights charges increased £214m primarily reflecting our investment in BT Sport Europe. Property and energy costs were up 7% and payments to telecommunications operators were up 2%, with these again being impacted by EE. Network operating and IT costs were up 1%. Net labour costs were flat despite leaver costs of £109m (2014/15: £8m), the additional EE employees joining the group and a £27m increase in the pensions operating charge. Underlying operating costs2 excluding transit were up 2%.

Adjusted EBITDA of £6,580m was up 5%.This included £261m from EE. Excluding foreign exchange movements and the effect of acquisitions and disposals, underlying EBITDA was up 1%.

Depreciation and amortisation increased 4% to £2,630m largely due to £176m from EE. Adjusted net finance expense was £483m, down 14% reflecting a lower weighted average interest rate and lower average net debt during the year.

Adjusted profit before tax was £3,473m, up 9%. Reported profit before tax (which includes specific items) was £3,029m, up 15%. The effective tax rate on the profit before specific items for the year was 17.5% (2014/15: 19.9%).

Adjusted EPS of 33.2p was up 5%. Reported EPS (which includes specific items) was 29.9p, up 13%. These are based on a weighted average number of shares in issue of 8,619m, up 7% reflecting the additional shares we have issued as part of the EE acquisition.

Specific items (see also Note 4)

Specific items resulted in a net charge after tax of £278m (2014/15: £406m). Specific items charged to revenue include £70m in relation to the unwind of an EE acquisition fair value adjustment on deferred income, and is a non-cash item. We have also incurred £124m (2014/15: £26m) of EE acquisition-related costs. Of these £99m (2014/15: £19m) were recognised in operating costs and were primarily advisor fees and stamp duty, and £8m (2014/15: £7m) were in financing costs. An additional £3m was directly related to the shares we issued to EE’s previous shareholders in January 2016 as part of the purchase consideration, so we have recognised this amount in equity. We’re treating operating costs relating to the integration as specific items and incurred £17m this year. In addition to this, £5m of integration expenditure has been capitalised.

We recognised a £29m property rationalisation cost. We also recognised £203m of both transit revenue and costs, with no EBITDA impact, being the effect of ladder pricing agreements relating to previous years following a Supreme Court judgment in 2014. Last year, we recognised specific revenue and EBITDA of £128m relating to this.

Net interest expense on pensions was £221m (2014/15: £292m). The tax credit on specific items was £70m (2014/15: £121m). We recognised a tax credit of £96m for the re-measurement of deferred tax balances due to the upcoming changes in the UK corporation tax rate from 20% to 19% from 1 April 2017 and to 18% from 1 April 2020.

Last year, specific items included a charge of £75m following an assessment of certain regulatory matters, restructuring charges of £315m, a £25m profit on disposal of an associate, a £22m net property rationalisation benefit, and a £6m net profit on the disposal of a number of small businesses.

1 Before specific items

2 Excludes specific items, foreign exchange movements and the effect of acquisitions and disposals and is before depreciation and amortisation

Capital expenditure

Capital expenditure was £2,650m (2014/15: £2,326m). This consists of gross expenditure of £2,759m (2014/15: £2,718m) which has been reduced by grants of £109m (2014/15: £392m) mainly relating to our activity on the Broadband Delivery UK (BDUK) programme. The total amount of grants recognised is lower than last year as we have deferred £229m of grant income due to strong levels of take-up. This year we increased our base-case assumption for take-up in BDUK areas (from 20% to 30% in the first quarter and again to 33% in the fourth quarter) and under the terms of the BDUK programme, we have a potential obligation to either re-invest or repay grant funding depending on factors including the level of customer take-up achieved. Without the impact of the deferral, our capital expenditure would have been £2,421m (2014/15: £2,297m). Much of this increase is due to EE which incurred £111m of capital expenditure in the period since acquisition.

Free cash flow

Normalised free cash flow1 was up £268m or 9% at £3,098m. The increase primarily reflects growth in EBITDA which includes £261m from EE trading. Normalised free cash flow excluding EE was £2,837m, in line with our outlook.

The net cash cost of specific items was £232m (2014/15: £154m) mainly comprising EE acquisition-related costs of £114m (2014/15: £nil), restructuring costs of £85m (2014/15: £267m) and ladder pricing receipts of £41m (2014/15: £88m). After specific items and a £203m (2014/15: £106m) tax benefit from pension deficit payments, reported free cash flow was £3,069m (2014/15: £2,782m).

We’ve provided a reconciliation of cash generated from operations to free cash flow in Note 5.

Net debt and liquidity

Net debt was £9,845m at 31 March 2016, an increase of £4,824m since 31 December 2015 and £4,726m higher than 31 March 2015. The increase in the year primarily reflects £3.5bn for the cash element of the EE acquisition, £2.1bn of acquired EE net debt, dividend payments of £1.0bn, pension deficit payments of £0.9bn and £315m for the buyback of 68m shares. These were partially offset by reported free cash flow of £3.1bn. In March we issued £3.0bn of euro denominated bonds to part-repay the £3.2bn drawdown on our £3.6bn committed acquisition facility. As at 31 March 2016, £0.2bn of the facility was still drawn down.

At 31 March 2016 the group held cash and current investment balances of £3.4bn. We have a £1.5bn facility which is undrawn and matures in September 2020.

Pensions (see also Note 11)

The IAS 19 net pension position at 31 March 2016 was a deficit of £5.2bn net of tax (£6.4bn gross of tax), compared with £4.9bn (£5.9bn gross of tax) at 31 December 2015 and £6.1bn (£7.6bn gross of tax) at 31 March 2015. The lower deficit relative to 31 March 2015 primarily reflects deficit payments of £880m (of which £875m relates to the BT Pension Scheme). The 31 March 2016 position includes a net deficit of £0.1bn for the defined benefit scheme operated by EE.

Based on the assumptions at 31 March 2016, the 2016/17 defined benefit pensions operating charge is expected to remain broadly unchanged from 2015/16, as a proportion of pensionable salary. A higher nominal discount rate is expected to reduce the net pension interest expense within specific items from £221m this year to around £210m for 2016/17.

Regulation

In February 2016 Ofcom published its initial conclusions on its Strategic Review of Digital Communications.

Ofcom set out three main conclusions:

- Openreach must make it easier for competitors to use its duct and poles to connect fibre to homes and offices;

- Openreach’s governance structure needs to be reformed to better serve UK consumers and businesses, with structural separation from BT a potential last resort; and

- End customers need a better quality of service, including automatic compensation.

We have made proposals to Ofcom for a voluntary agreement that would address Ofcom’s concerns and could be implemented quickly, avoiding a prolonged period of uncertainty for the industry. These proposals are centred around a new governance structure for Openreach. Many of Ofcom’s proposals are already in place, for example BT’s ducts and poles have been open to competitors since 2011.

1 Before specific items, pension deficit payments and the cash tax benefit of pension deficit payments

On 28 April 2016 Ofcom published its final Statement on its Business Connectivity Market Review, Leased Lines Charge Control and Cost Attribution Review. This broadly confirmed Ofcom’s proposals set out in its Draft Statement published in March, including:

- the charge controls to apply from 1 May 2016 until 31 March 2019;

- the introduction of minimum service levels for Openreach relating to the installation and repair of Ethernet services; and

- a requirement on Openreach to provide access to its fibre network for providers of high speed services to businesses (‘dark fibre’) from 1 October 2017.

We expect Ofcom’s Cost Attribution Review assessment to also have an effect on future price controls, including Wholesale Local Access and Narrowband.

BT has appealed Ofcom’s decision to introduce the VULA margin squeeze test to the Competition Appeals Tribunal (CAT). Our appeal argued that Ofcom had not met the legal or evidential tests to impose such a condition (as covered in ground one of our appeal), and also that Ofcom had erred in law, in fact and / or in the exercise of its discretion in setting the price control (grounds two to five). In March 2016 the CAT issued its judgment on ground one, finding that Ofcom was entitled to impose a regulatory margin squeeze test. Our appeal on the other grounds is being heard by the Competition and Markets Authority (CMA). The CMA’s final determination is expected in June or July and it will be subject to ratification by the CAT later in the summer.

In January 2016, we appealed to the CAT about Ofcom’s November 2015 decision to remove Sky’s wholesale must offer obligation on Sky Sports. We believe that effective remedies are essential to address the failure of competition in the pay-TV market, where Sky has held a dominant position for more than a decade. We expect the hearing to be held in October 2016.

Dividends

The Board is proposing a final dividend of 9.6p, up 13%, giving a full year dividend of 14.0p, also up 13%. Subject to shareholder approval, this will be paid on 5 September 2016 to shareholders on the register at 12 August 2016. The ex-dividend date is 11 August 2016. The final dividend, amounting to approximately £956m (2014/15: £712m), will be recognised as an appropriation of retained earnings in the quarter to 30 September 2016.

Principal risks and uncertainties

The group’s principal risks and uncertainties are disclosed in Note 12.

Outlook

We expect growth in underlying revenue excluding transit in 2016/17. Adjusted EBITDA is expected to be around £7.9bn, after a net investment of around £100m in launching handset offerings to BT Mobile customers. Normalised free cash flow is expected to be £3.1bn - £3.2bn. This is after up to £300m of upfront capital expenditure in relation to the Emergency Services Network (ESN) contract, as well as around £100m of EE integration capital expenditure.

For 2017/18, we expect growth in underlying revenue excluding transit and adjusted EBITDA. We also expect to incur capital expenditure of around £100m on the ESN contract and around £100m again on integration. We are confident in our cash flow generation as a result of the investments we are currently making, the ability of our business to respond to a dynamic industry environment, and ongoing cost transformation and synergy realisation opportunities. As such, we expect to generate normalised free cash flow of more than £3.6bn in 2017/18.

We expect to grow our dividend per share by at least 10% in both 2016/17 and 2017/18. We expect to buy back around £200m of shares in 2016/17 to help counteract the dilutive effect of all-employee share option plans maturing in the year. This is below the £315m buyback we completed in 2015/16 reflecting the lower number of shares that are expected to be required for our share option plans.

GROUP RESULTS FOR THE FOURTH QUARTER TO

31 MARCH 2016

Income statement

Our financial performance in the quarter has been significantly impacted by the inclusion of EE for two months. Revenue of £5,656m was up 22% with a £1,038m contribution from EE, a £27m positive impact from foreign exchange movements and a £22m reduction in transit revenue.

Underlying revenue excluding transit was up 1.3%, reflecting 8% growth in BT Consumer, 2% in Openreach and 2% in BT Business. These more than offset the underlying revenue excluding transit declines in our other lines of business, with BT Wholesale down 8%, reflecting the benefit of ladder pricing revenue recognised last year, and BT Global Services down 2%.

Adjusted operating costs1 were up £760m or 27%. Of this £725m relates to EE with a large proportion within Other costs. These were up £342m or 38% for the group, primarily reflecting EE’s subscriber acquisition and retention costs. Net labour costs increased £133m or 14% reflecting the additional EE employees joining the group. Payments to telecommunications operators were up £128m or 25%. Programme rights charges were up £76m primarily reflecting our investment in BT Sport Europe. Property and energy costs and network, operating and IT costs were also up £62m and £19m respectively, mainly reflecting the impact from EE.

Adjusted EBITDA increased 14% to £2,076m of which EE contributed £261m. Excluding foreign exchange movements and the effect of acquisitions and disposals, underlying EBITDA was down 1% reflecting the ladder pricing benefit last year. Underlying operating costs2 excluding transit were up 2%.

Depreciation and amortisation of £787m was up 21%. Adjusted net finance expense was £144m, an increase of 4% reflecting the higher average net debt in the quarter as a result of the acquisition of EE.

Adjusted profit before tax was £1,145m, up 11%. Reported profit before tax (which includes specific items) was £893m, up 6%. The effective tax rate on the profit before specific items for the quarter was 15.1% (Q4 2014/15: 19.9%). Adjusted EPS of 10.2p was up 2%. Reported EPS (which includes specific items) was 8.0p, down 5%. These are based on a weighted average number of shares in issue of 9,457m (Q4 2014/15: 8,221m).

Specific items (see also Note 4)

Specific items in the quarter resulted in a net charge after tax of £216m (Q4 2014/15: £135m). Specific items charged to revenue include £70m in relation to the unwind of the EE acquisition adjustment on deferred income. We recognised EE acquisition-related fees of £82m (Q4 2014/15: £19m) in the quarter as specific operating costs, with a further £3m (Q4 2014/15: £10m) recognised in equity and £5m (Q4 2014/15: £7m) as a finance expense. We’re treating operating costs relating to the integration as specific items and incurred £11m this quarter.

We also recognised a £29m property rationalisation cost. Net interest expense on pensions was £55m (Q4 2014/15: £74m). The tax credit on specific items was £34m (Q4 2014/15: £53m).

Last year, specific items included restructuring charges of £157m, a £22m charge following an assessment of certain regulatory matters, and a £22m net property rationalisation benefit.

Capital expenditure

Capital expenditure was £776m, up 14% primarily reflecting £111m from EE. This is after £61m of gross grant funding mainly relating to our activity on the BDUK programme. This was offset by the deferral of £79m of the total grant funding we have accrued to date.

Free cash flow

Normalised free cash flow was £1,519m, up 20%. This reflects the growth in EBITDA of £257m, including EE’s contribution. The movement was offset by tax payments and the timing of working capital. The cash cost of specific items was £132m (Q4 2014/15: £3m). Free cash flow, which includes specific items and a £44m (Q4 2014/15: £53m) tax benefit from pension deficit payments, was £1,431m (Q4 2014/15: £1,317m).

1 Before depreciation and amortisation

2 Excludes specific items, foreign exchange movements, the effect of acquisitions and disposals and is before depreciation and amortisation

OPERATING REVIEW

BT Global Services

Revenue declined 2% in the quarter with a £24m positive impact from foreign exchange movements and a £3m decline in transit revenue. Underlying revenue excluding transit also decreased 2% primarily reflecting lower revenue in the UK and in the US and Canada. For the year, revenue declined 4% including a £105m negative impact from foreign exchange movements and a £30m decline in transit revenue. Underlying revenue excluding transit declined 2% for the year, an improvement on the 4% decline the year before.

Revenue in the UK was down 2% for the quarter primarily reflecting lower public sector revenue. In the high-growth regions1 underlying revenue excluding transit was flat for the quarter. This was below the growth rate in the third quarter due to the timing of milestone-related revenue in the AMEA2 region within the year. For the full year underlying revenue excluding transit grew 12% in AMEA. In the US and Canada underlying revenue excluding transit declined 13% for the quarter reflecting the ongoing impact of a major customer insourcing services. In Continental Europe underlying revenue excluding transit was up 2%. We have seen very strong demand for our cyber security expertise with our security business growing by 24%.

Total order intake was £1.5bn in the quarter, down 25% after last year benefited from some large contract re-signs. For the year, order intake was down 4% to £6.2bn. Excluding renewals, the order intake grew in the year. In the quarter, we signed a contract with Kingfisher, which owns B&Q and Screwfix, for network services in the UK. In Continental Europe we signed a contract with Nexans for network services in 40 countries, including voice and data, fixed and mobile, security and cloud-based collaboration services. We also signed a contract with Panalpina, one of the world’s leading freight and logistics companies, to transform and manage their global communications infrastructure for 15,000 employees in more than 75 countries. In Australia, we signed a contract with ALS for a global managed network comprising WAN services, internet access, cloud connectivity, network acceleration and optimisation as well as managed security services.

During the quarter, we launched BT Connect Intelligence IWAN, an SDN capability that helps customers to better manage their network traffic and secure their business applications. Building on our Cloud of Clouds strategy, our Cloud Connect customers can now connect directly to Salesforce’s Customer Success Platform. We also announced an agreement to work with Intel Security to develop new solutions that help organisations improve security and prevent cyber-attacks.

Operating costs declined 4% for the quarter and for the year. Underlying operating costs excluding transit were down 4% for the quarter and 1% for the year reflecting the impact of lower revenue and the benefit of our cost transformation programmes partly offset by a change in margin mix and higher leaver costs.These were £5m in the quarter (Q4 2014/15: £nil) and £25m for the year (2014/15: £nil). EBITDA in the quarter was up 5% and was flat for the year. Excluding foreign exchange movements, underlying EBITDA was up 1% in the quarter and for the year. Depreciation and amortisation was up 13% in the quarter due to the timing of recognition on certain contracts and operating profit of £222m was up 1%.

Capital expenditure declined 4% in the quarter, and 11% in the year, largely reflecting improved efficiencies. Operating cash flow was an inflow of £545m for the quarter (Q4 2014/15: £599m), and £475m for the year. This was an increase of £126m benefiting from timing of contract-specific cash flows and the lower capital expenditure.

1 Asia Pacific, the Middle East and Africa (AMEA) and Latin America

2 Asia Pacific, the Middle East and Africa (AMEA)

BT Business

Revenue and underlying revenue excluding transit were up 2% for the quarter, and broadly flat for the year.

SME & Corporate voice revenue was up 1% for the quarter, with higher average revenue per user and higher take-up of VoIP services offsetting the continued fall in business line volumes. The number of traditional lines declined 7%, in line with last quarter, but this was partly offset by a 62% increase in the number of IP lines.

SME & Corporate data and networking revenue increased 1% and IT services revenue declined 1%. BT Ireland underlying revenue excluding transit was up 3% driven by a one-off contract benefit as well as higher call and data volumes in the Republic of Ireland, growth in managed services and continued fibre broadband growth in Northern Ireland. Foreign exchange movements had a £3m positive impact on BT Ireland revenue in the quarter. Other revenue increased 10% due to pricing changes in BT Directories.

Order intake in the quarter decreased 21% to £481m and was down 5% to £1,967m for the year, after last year included a number of large deals such as Primark Stores and Shaw Trust.

Deals signed in the quarter include a new three-year agreement with Equiniti to extend network services, deliver a substantial upgrade to their data network and improve security. Pets at Home purchased new electronic points of sale as part of an upgrade programme for both new stores and their 435 existing stores. In Ireland we signed a deal with Blacknight Internet Solutions to provide data centre, network and infrastructure services.

BT Cloud Voice (our business-grade IP voice service) and BT Cloud Phone (a 'plug and play' IP phone system) continue to perform well. Since the start of the quarter, the number of BT Cloud Voice users increased 29% and the number of BT Cloud Phone users increased 34%.

Our Call Essentials package, aimed at small UK businesses with up to 50 phone lines, is also performing well. We have signed up over 80,000 customers since its launch in the first quarter.

Operating costs on both a reported and underlying basis were down 3% for the quarter and 2% for the year, as a result of our cost transformation activities. EBITDA grew 3% for the year and 11% for the quarter, partly due to the one-off contract benefit in Ireland. Depreciation and amortisation increased £7m for the quarter and operating profit grew 10%.

Capital expenditure decreased £58m for the quarter and £49m for the year mainly due to the investment we made last year in BT Fleet vehicles to support Openreach. Operating cash flow was 6% higher in the quarter reflecting the lower capital expenditure. For the year operating cash flow was down 6%, with the lower capital expenditure more than offset by the timing of working capital movements.

BT Consumer

Revenue for the quarter was up 8% with a 20% increase in broadband and TV revenue and a 2% increase in calls and lines revenue. For the year, revenue was up 7%. Consumer ARPU increased 7% to £446 driven by broadband, our new BT Sport Europe channels and BT Mobile.

Excluding EE, BT added 94,000 retail broadband customers in the quarter, representing 72% of the DSL and fibre broadband market net additions. Superfast fibre broadband growth continued with 204,000 retail net additions, taking our customer base to 3.9m. Of our broadband customers, 48% are now on fibre.

Our consumer line losses of 18,000, were lower than the prior year (Q4 2014/15: 61,000) but higher than the third quarter as a result of lower broadband sales. In the quarter we announced a free service to combat nuisance calls which will be launched later in the calendar year. By harnessing computing power to analyse large amounts of live data the service will enable customers to divert up to 25 million unwanted calls a week to a junk voicemail box.

We have continued to build on the success of our BT Mobile launch with over 400,000 SIM-only customers signed up to date and customer satisfaction higher than for any other BT Consumer product. As a result of the progress to date and the good demand for the product, next year we will be launching handset offerings to BT Mobile customers. We expect this investment to negatively impact our EBITDA by around £100m in the year.

BT Sport’s average daily audience figures, from the start of the football season in August to the end of March, increased 45% year on year. For the same period, we saw 39 match events with peak concurrent viewers of over 1m. And the UEFA Europa League last 16 first leg clash between Liverpool and Manchester United generated a peak of more than 2m viewers, the first time we’ve hit this milestone.

We added 66,000 TV customers, taking the base to 1.5m customers. In the quarter we launched a new version of the TV app with a new, dedicated kids on-demand and catch-up library, seven more channels and a collection of premium entertainment catch-up content.

We have continued to invest in improving the customer experience and our target is now to answer 90% of BT Consumer customers’ calls from within the UK by the end of March 2017. We have already filled more than 900 new roles in our UK contact centres and this quarter announced that we will create an additional 1,000 permanent UK contact centre roles between now and April 2017. We have also announced that from July all our standard line rental customers will receive a faster repair service with any faults fixed 24 hours sooner. And customers with Infinity 1 broadband will see their speeds increase from up to 38Mbps to up to 52Mbps.

Operating costs increased 13% in the quarter and 9% for the year due to costs relating to the first season of our BT Sport Europe channels. EBITDA declined 2% in the quarter but was up 1% for the year. Depreciation and amortisation was down 19% in the quarter and operating profit was up 2%.

Capital expenditure declined 25% in the quarter mainly as a result of lower BT Sport studio costs. Despite this, operating cash flow decreased 28% as a result of working capital movements relating to the timing of our BT Sport Europe rights payments. For the year capital expenditure was flat and operating cash flow decreased by 6%.

EE

Revenue for the two months since we acquired EE was £1,055m. This consists of mobile service revenue of £913m, fixed and wholesale revenue of £89m and equipment sales of £53m. Of total revenue, £1,038m was external and £17m was internal. Monthly mobile ARPUs in the period were £26.7 for postpaid customers, £3.9 for prepaid and £18.6 on a combined basis.

At the end of the period the total customer base was 30.6m (excluding BT Mobile customers). EE added 54,000 postpaid mobile customers in the two months, taking the postpaid customer base to 15.4m. We signed a number of significant corporate customers including Arriva Trains, and we began connecting users under our Anglian Water and Prudential contracts. The number of prepaid customers reduced by 426,000 taking the base to 8.3m, with a seasonal drop following Christmas trading, faster migrations to postpaid and greater price competition from the MVNO market. The 4G customer base reached 15.1m. The MVNO base and machine to machine bases increased by 28,000 and 77,000 over the two months to 3.7m and 2.3m respectively. EE added 11,000 broadband customers taking the base to 951,000 and customers choosing to take fibre broadband grew by 10,000. Postpaid churn was 1.1% reflecting the high level of customer loyalty.

We were again recognised as the leading UK mobile network, with Rootmetrics naming EE as having the best overall mobile network. We also won the Speedtest fastest mobile network award in the period. We’re making good progress with extending our network, with 4G calling now available in Bristol, Hatfield, Birmingham, Manchester, Edinburgh and Belfast.

On 25 April we announced plans for 100% of customer service calls to be handled in the UK and Ireland by the end of 2016. We also announced plans to extend our 4G geographic coverage to 95% of the UK by 2020, from 60% today, significantly increasing the availability of 4G in even the most remote locations.

Operating costs were £794m (of which £69m were internal charges from other parts of the group) resulting in EBITDA of £261m, an EBITDA margin of 25%.

Capital expenditure was £111m as we extended 4G coverage to over 96% of the UK population. Preparation for the Emergency Services Network contract continued in line with agreed milestones.

Operating cash flow of £310m (which excludes interest or tax) benefited from working capital movements.

1 The period from the acquisition of EE on 29 January 2016 to 31 March 2016

BT Wholesale

For the quarter revenue was 11% lower with underlying revenue excluding transit down 8%.This reflects the benefit last year of around £30m of revenue related to ladder pricing that we recognised in the fourth quarter. For the year revenue declined 3% with underlying revenue excluding transit up 1%. This is an improvement on the 7% decline the year before reflecting growth in IP services and Managed Solutions, partly offset by a decline in our traditional calls and lines revenues.

Calls, lines and circuits revenue was down 36% in the quarter mainly reflecting the ladder pricing benefit last year and lower volumes with customers switching to newer IP technologies. Managed Solutions revenue was down 4% in the quarter due to lower connection volumes.

Broadband revenue was down 5%.This was an improvement on last year’s decline of 16% for the quarter. While the migration of lines to LLU continues to reduce the copper base, fibre volumes continue to increase, reflecting demand across the market.

IP services revenue was up 26% in the quarter, largely driven by growth in IP Exchange minutes, which were up 30%. In addition, Ethernet continued to grow strongly with a 23% increase in the rental base.

During the quarter the BBC chose BT to provide its next generation broadcast network in a deal worth more than £100m to BT. This will enable the BBC to move to a new, state of the art network from April 2017. Order intake in the quarter was £454m down from £956m last year. For the year it was £1,505m, down around £400m on last year’s order intake, but up around £150m excluding orders signed with EE.

Operating costs decreased 7% in the quarter. Underlying operating costs excluding transit reduced 2% reflecting lower cost of sales and the benefit of our cost transformation activities. We reduced selling and general administration costs 7% in the quarter.

EBITDA decreased 20% in the quarter mainly due to the ladder pricing benefit last year and decreased 3% for the year. Depreciation and amortisation decreased 8% in the quarter. Operating profit decreased 25% in the quarter and 2% for the year.

Capital expenditure was £9m lower in the quarter, and down £33m for the year driven by lower spend on sustaining our legacy voice network and because last year included some investments on efficiency programmes.

Operating cash flow was up £11m for the quarter and £126m for the year, with working capital helped by better collections.

Openreach

Revenue increased 2% in the quarter and 2% for the year. Regulatory price changes had an overall negative impact of around £30m in the quarter, equivalent to 2% of revenue, and around £130m in the year. In the quarter this was more than offset by 32% growth in fibre broadband revenue.

The UK broadband market1 increased by 130,000 connections in the quarter compared with 248,000 in the prior year. The physical line base reduced by 29,000 in the quarter but has remained broadly flat over the year.

We achieved 415,000 fibre broadband net additions in the quarter. This was the third highest on record but lower than last year, which had been a record quarter at the time. There are now 5.9m homes and businesses connected to our fibre broadband network, 23% of those passed. Other service providers added 201,000, or just under half of the net connections in the quarter, demonstrating consistent market-wide demand for fibre.

During the quarter, Openreach hit the milestone of bringing fibre broadband to more than 25m premises across the UK. Together with other networks, this means 90% of the UK is able to enjoy fibre broadband speeds. Openreach is building on its G.fast technology trials with two new pilot sites in Cambridgeshire and Kent. 25,000 homes and businesses in these areas will be able to access download speeds of up to 330Mbps using G.fast from their nearest street cabinet. Openreach will also be conducting two trials of business Fibre-to-the-Premises (FTTP) in Bradford, providing ultrafast speeds of up to 1Gbps.

We achieved all 60 of the minimum service levels set by Ofcom for the installation of new lines and for repairs to existing services. This performance is despite the operational pressures of the severe weather and flooding during the year, particularly in January.

Operating costs grew 4% in the quarter, mainly reflecting more repair work to rectify the impact of the floods. There was also no benefit this year from the sale of redundant copper (2014/15: Q4 £6m and full year £29m). EBITDA was flat in the quarter and with depreciation and amortisation 4% lower, operating profit was up 4%. EBITDA increased by 2% for the year.

Capital expenditure was £376m, up £98m or 35%.This was after gross grant funding of £54m (Q4 2014/15: £127m) directly related to our fibre broadband network build in the quarter. The total amount of grants recognised is lower than last year as we have deferred £78m of grant income due to strong levels of take-up. This is primarily because we increased our base-case assumption for take-up from 30% to 33% and under the terms of the BDUK programme, we have a potential obligation to either re-invest or repay grant funding depending on factors including the level of customer take-up achieved. Excluding the impact of grants, gross capital expenditure was £352m (Q4 2014/15: £394m).

For the year, capital expenditure grew 34%, reflecting the deferral of £227m of grant funding together with the investments in connecting new homes and businesses, and in Ethernet. Excluding the impact of grants, gross capital expenditure grew 5% and we expect it to grow again in 2016/17.

Operating cash flow increased by 2% in the quarter largely due to the timing of customer receipts. It was down 6% for the year, primarily reflecting the higher capital expenditure.

1 DSL and fibre

We will hold the fourth quarter and full year 2015/16 results presentation for analysts and investors in London at 9.30am today and a simultaneous webcast will be available at www.bt.com/results

We expect to publish the BT Group plc Annual Report & Form 20-F 2016 on 19 May 2016. The Annual General Meeting of BT Group plc will be held at The Motorpoint Arena, Mary Ann Street, Cardiff, CF10 2EQ, on 13 July 2016 at 10:30am.

We expect to announce our results for the first quarter to 30 June 2016 on 28 July 2016.

Categories

- shareholders

- financial results

About BT

BT’s purpose is to use the power of communications to make a better world. It is one of the world’s leading providers of communications services and solutions, serving customers in 180 countries. Its principal activities include the provision of networked IT services globally; local, national and international telecommunications services to its customers for use at home, at work and on the move; broadband, TV and internet products and services; and converged fixed-mobile products and services.With effect from 1 April 2016, the group has been reorganised and the customer-facing lines of business are now: Global Services, Business and Public Sector, Consumer, EE, Wholesale and Ventures, and Openreach.

For the year ended 31 March 2016, BT Group’s reported revenue was £19,042m with reported profit before taxation of £3,029m.

British Telecommunications plc (BT) is a wholly-owned subsidiary of BT Group plc and encompasses virtually all businesses and assets of the BT Group. BT Group plc is listed on stock exchanges in London and New York.

For more information, visit www.btplc.com

BT News