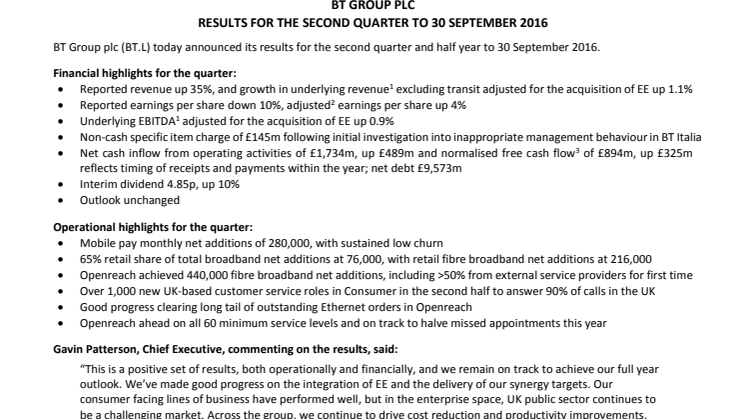

Press release -

Results for the second quarter to 30 September 2016

BT Group plc (BT.L) today announced its results for the second quarter and half year to 30 September 2016.

Financial highlights for the quarter:

- Reported revenue up 35%, and growth in underlying revenue1 excluding transit adjusted for the acquisition of EE up 1.1%

- Reported earnings per share down 10%, adjusted2 earnings per share up 4%

- Underlying EBITDA1 adjusted for the acquisition of EE up 0.9%

- Non-cash specific item charge of £145m following initial investigation into inappropriate management behaviour in BT Italia

- Net cash inflow from operating activities of £1,734m, up £489m and normalised free cash flow3 of £894m, up £325m reflects timing of receipts and payments within the year; net debt £9,573m

- Interim dividend 4.85p, up 10%

- Outlook unchanged

Operational highlights for the quarter:

- Mobile pay monthly net additions of 280,000, with sustained low churn

- 65% retail share of total broadband net additions at 76,000, with retail fibre broadband net additions at 216,000

- Openreach achieved 440,000 fibre broadband net additions, including >50% from external service providers for first time

- Over 1,000 new UK-based customer service roles in Consumer in the second half to answer 90% of calls in the UK

- Good progress clearing long tail of outstanding Ethernet orders in Openreach

- Openreach ahead on all 60 minimum service levels and on track to halve missed appointments this year

Gavin Patterson, Chief Executive, commenting on the results, said:

“This is a positive set of results, both operationally and financially, and we remain on track to achieve our full year outlook. We’ve made good progress on the integration of EE and the delivery of our synergy targets. Our consumer facing lines of business have performed well, but in the enterprise space, UK public sector continues to be a challenging market. Across the group, we continue to drive cost reduction and productivity improvements. Customer experience remains a key priority, and we’re stepping up our investments in the second half of the year. And we’ll continue to invest in our ultrafast and 4G plans in 2017 and beyond. Ofcom’s consultation on the Digital Communications Review closed earlier this month; we’ve submitted our response and will continue to engage with Ofcom to reach the best outcome for the UK.”

1 Excludes specific items, foreign exchange movements and disposals and is calculated as though EE had been part of the group from 1 April 2015. This differs from how we usually adjust for acquisitions as explained on page 3

2 Before specific items, which are defined on page 3

3 Before specific items, pension deficit payments and the cash tax benefit of pension deficit payments

4 The results for the period include EE which we acquired on 29 January 2016. Unless referred to as underlying adjusted for the acquisition of EE, comparatives do not include EE

GROUP RESULTS FOR THE SECOND QUARTER AND HALF YEAR TO 30 SEPTEMBER 2016

Line of business results2

1 The results for the period include EE which we acquired on 29 January 2016. Unless referred to as underlying adjusted for the acquisition of EE, comparatives do not include EE

2 Before specific items, which are defined on page 3

3 Excludes specific items, foreign exchange movements and disposals and is calculated as though EE had been part of the group from 1 April 2015. This differs from how we usually adjust for acquisitions as explained on page 3

4 Before specific items, pension deficit payments and the cash tax benefit of pension deficit payments

5 Certain line of business results have been restated. See Note 1 to the condensed consolidated financial statements

n/m = not meaningful

Notes:

- Our commentary focuses on the trading results on an adjusted basis, which is a non-GAAP measure, being before specific items. Unless otherwise stated, revenue, operating costs, earnings before interest, tax, depreciation and amortisation (EBITDA), operating profit, profit before tax, net finance expense, earnings per share (EPS) and normalised free cash flow are measured before specific items. This is consistent with the way that financial performance is measured by management and reported to the Board and the Operating Committee and assists in providing a meaningful analysis of the trading results of the group. The directors believe that presentation of the group’s results in this way is relevant to the understanding of the group’s financial performance as specific items are those that in management’s judgement need to be disclosed by virtue of their size, nature or incidence. In determining whether an event or transaction is specific, management considers quantitative as well as qualitative factors such as the frequency or predictability of occurrence. Specific items may not be comparable with similarly titled measures used by other companies. Reported revenue, reported operating costs, reported operating profit, reported profit before tax, reported net finance expense and reported EPS are the equivalent unadjusted or statutory measures. Reconciliations of reported to adjusted revenue, operating costs and operating profit are set out in the Group income statement. Reconciliations of underlying revenue excluding transit adjusted for the acquisition of EE, underlying operating costs excluding transit adjusted for the acquisition of EE, EBITDA, underlying EBITDA adjusted for the acquisition of EE, net debt and free cash flow to the nearest measures prepared in accordance with IFRS are provided in the notes to the condensed consolidated financial statements and in the Additional information.

- Trends in underlying revenue excluding transit adjusted for the acquisition of EE, underlying operating costs excluding transit adjusted for the acquisition of EE, and underlying EBITDA adjusted for the acquisition of EE are non-GAAP measures which seek to reflect the underlying performance of the group that will contribute to long-term sustainable growth and as such exclude the impact of acquisitions and disposals, foreign exchange movements and any specific items. We exclude transit from the trends as transit traffic is low-margin and is affected by reductions in mobile termination rates. Given the significance of the EE acquisition to the group, in 2016/17 we are calculating underlying revenue excluding transit adjusted for the acquisition of EE, underlying operating costs excluding transit adjusted for the acquisition of EE and underlying EBITDA adjusted for the acquisition of EE (see note 3), as though EE had been part of the group from 1 April 2015. This is different from how we usually adjust for acquisitions, and is the basis for our 2016/17 outlook.

- We have prepared and published historical financial information adjusted for the acquisition of EE (previously described as pro forma historical financial information) for the eight quarters ended 31 March 2016 for the group and by line of business under our new organisational structure, to illustrate the results as though EE had been part of the group from 1 April 2014. This historical financial information adjusted for the acquisition of EE shows EE’s historical results adjusted to reflect BT’s accounting policies. In the consolidated group total, we’ve eliminated historical transactions between BT and EE as though they had been intercompany transactions. We’ve not made any adjustments to reflect the allocation of the purchase price for EE. And all deal and acquisition-related costs have been treated as specific items and therefore don’t impact the published information.

BT Group plc

GROUP RESULTS FOR THE QUARTER TO 30 SEPTEMBER 2016

Note: The results for the period include EE which we acquired on 29 January 2016. Unless referred to as underlying adjusted for the acquisition of EE, the comparatives do not include EE as explained in the notes on page 3.

Overview

We’re pleased with our performance in the quarter. Our key measure of the group’s revenue trend, underlying revenue1 excluding transit adjusted for the acquisition of EE, was up 1.1%. Consumer revenue was up 11%, with broadband and TV revenue up 17%. Global Services underlying revenue1 excluding transit adjusted for the acquisition of EE was up 3% partly reflecting a large one-off benefit from equipment sales and strong IP Exchange volumes. EE underlying revenue1 adjusted for the acquisition of EE and Openreach revenue were both flat, with continued strong growth in 4G and fibre, respectively, offsetting the impact of regulatory price changes. Wholesale and Ventures underlying revenue1 excluding transit adjusted for the acquisition of EE was down 5%, as a result of the decline in Partial Private Circuits and call volumes. Business and Public Sector underlying revenue1 excluding transit adjusted for the acquisition of EE was down 7%, due to the ongoing completion of a number of public sector contracts.

Underlying operating costs1,2 excluding transit adjusted for the acquisition of EE were up 1%. As we’ve previously disclosed, this reflects additional UEFA rights costs and the increased investment in mobile handsets. Without these items, underlying operating costs1,2 excluding transit adjusted for the acquisition of EE were flat. Underlying EBITDA1 adjusted for the acquisition of EE was up 0.9%, with growth in Consumer offset by declines in Business and Public Sector, Openreach, EE and Wholesale and Ventures. And we remain on track to meet our synergy targets in relation to the integration of EE.

Our TV customer base continues to grow. During the quarter we added 63,000 new customers taking our base to 1.7m. And at BT Sport, we are benefiting from our new Saturday early evening slot for Premier League matches, with better viewing figures than last year.

Our mobile base of 30.2m was consistent with last quarter. We added 280,000 postpaid mobile customers, taking the postpaid customer base to 16.4m. The number of prepaid customers reduced by 325,000, in line with industry trends, taking the base to 7.6m. The 4G customer base reached 17.6m. Monthly mobile ARPUs3 were £27.4 for postpaid customers, and £4.4 for prepaid customers. We’ve maintained EE’s postpaid churn at a record low of 1.0% which reflects continued strong customer loyalty.

The UK broadband market4 grew by 116,000, of which our retail share was 76,000 or 65%. Retail fibre broadband demand was strong as ADSL customers continue to move across to fibre. We added 216,000 customers this quarter, taking our base to 4.5m. Openreach achieved 440,000 fibre broadband net connections wth service providers other than BT more than 50%, for the first time. This brings the number of homes and businesses connected to around 6.7m, 26% of those passed.

Investing in our network and customer experience

We’ve passed over 26m premises with our superfast fibre broadband network. In total, this means 92% of the UK now has access to fibre broadband from BT or other networks. We remain on track to help bring fibre broadband to 95% of the country by the end of 2017, with plans to go even further. Our plans to make ultrafast broadband available to up to 12m premises by the end of 2020 are also progressing well and we will soon extend our G.fast pilots to another 12 locations. This means our ultrafast network will pass 500,000 premises by April 2017.

We’ve doubled the speed of BT Infinity for business customers, migrating existing connections to our new standard download speed of up to 76Mbps where technically possible. And our average Consumer customer broadband speeds have increased by more than 18% compared to the same period last year.

We’re making progress on our strategy to reach 92% 4G geographic coverage by September 2017 and 95% by the end of December 2020. At 30 September 2016 we had reached UK geographic coverage of 70% (98% 4G population coverage), with the widest coverage of any UK operator. During the quarter EE launched the next phase of the 4G+ network, capable of providing real world speeds of over 360Mbps, which will be deployed on 500 sites across the UK by the end of 2017.

1Excludes specific items, foreign exchange movements and disposals and is calculated as though EE had been part of the group from 1 April 2015. This differs from how we usually adjust for acquisitions as explained on page 3

2Before depreciation and amortisation

3Consistent with EE Limited ARPU calculation and excludes Consumer mobile customers, who are included in the Consumer ARPU calculation

4DSL and fibre, excluding cable

We continue to focus on customer experience. We’re adding over 1,000 UK-based customer service roles in the second half of the year in Consumer as part of our commitment to answer 90% of calls in the UK by the end of March. Since July, EE has answered 100% of EE postpaid calls in UK and Ireland contact centres, and we continue to progress towards our target of handling all EE customer calls in the UK and Ireland by the end of December. In Consumer we’re now fixing customer voice faults on average one day sooner. And in Openreach we’ve reduced the number of appointments our engineers miss and are on track to halve missed appointments by the end of the financial year.

The UK’s exit from the EU

The weakening of Sterling has continued to impact our financial results. While the future nature of Britain’s trading relationship with the EU and globally is currently uncertain, the Board does not expect the result of the EU referendum to have a significant impact on our outlook, which remains unchanged. We continue to monitor the longer term impact of the UK’s decision to exit the EU.

Income statement

Reported revenue was £6,007m, up 35%. Adjusted revenue, which is before specific items, was £6,053m, up 38%, mainly as a result of the contribution of EE. This includes a £154m favourable impact from foreign exchange movements, and a £2m reduction in transit revenue. Underlying revenue1 excluding transit adjusted for the acquisition of EE was up 1.1%.

Reported operating costs were up 41% and adjusted operating costs2 were up 42% at £4,165m, due mainly to EE. Underlying operating costs1,2 excluding transit adjusted for the acquisition of EE were up 1%. Net labour costs of £1,220m were up 16%, reflecting the additional EE employees that have joined the group as well as leaver costs of £14m.

Property and energy costs were up 28%, network operating and IT costs up 44% and payments to telecommunications operators up 30%, driven primarily by EE. BT Sport programme rights charges were £177m, up £42m mainly as a result of UEFA rights charges. Other costs were up £721m or 89%, reflecting EE.

Adjusted EBITDA of £1,888m was up 31%. Underlying EBITDA1 adjusted for the acquisition of EE was up 0.9%. Depreciation and amortisation of £869m was up 39% largely due to the impact of EE. Reported net finance expense was £199m while adjusted net finance expense was £146m, up £34m primarily due to higher net debt as a result of our acquisition of EE.

Reported profit before tax (which includes specific items) was £671m, up 5%. Adjusted profit before tax increased 24% to £873m. The effective tax rate on profit before specific items was 17.9% (Q2 2015/16: 18.3%).

Reported EPS (which includes specific items) was 5.7p, down 10%. Adjusted EPS of 7.2p was up 4%. These are based on a weighted average number of shares in issue of 9,932m (Q2 2015/16: 8,339m), up 19% mainly reflecting the additional shares we issued as part of our acquisition of EE.

Specific items

Specific items resulted in a net charge after tax of £151m (Q2 2015/16: £52m charge). See Note 4 for a breakdown.

BT Italia investigation

Following allegations of inappropriate management behaviour in our BT Italia operations, we have conducted an initial internal investigation. This included a review of accounting practices during which we have identified certain historical accounting errors and reassessed certain areas of management judgement.

We have written down the value of items on the balance sheet by £145m. This is our current best estimate of the financial impact based on our internal investigation. The write down relates to balances that have built up over a number of years and our assessment is that the errors have not materially impacted the group’s reported earnings over the previous two years. The amount has been charged as a specific item in our results for the quarter. As a non-cash item in the period it does not impact normalised free cash flow.

A full investigation of these matters is ongoing and we have appointed external advisers to assist with this. Appropriate action will be taken as the investigation progresses.

Our outlook is not affected.

1 Excludes specific items, foreign exchange movements and disposals and is calculated as though EE had been part of the group from 1 April 2015. This differs from how

we usually adjust for acquisitions as explained on page 3

2 Before depreciation and amortisation

Other specific items

Other specific items reflect EE integration costs of £18m (Q2 2015/16: EE acquisition-related costs £8m), net interest expense on pensions of £53m (Q2 2015/16: £56m) and a profit on disposal of a business of £14m (Q2 2015/16: £nil). We also recognised £6m (Q2 2015/16: £78m) of both transit revenue and costs, with no EBITDA impact, being the effect of ladder pricing agreements relating to previous years. The tax credit on specific items was £8m (Q2 2015/16: £12m). We also recognised a tax credit of £43m for the re-measurement of deferred tax balances due to the UK corporation tax rate reduction (18% to 17%) effective from 1 April 2020.

Capital expenditure

Capital expenditure was £802m (Q2 2015/16: £629m). This consists of gross expenditure of £815m (Q2 2015/16: £691m) which has been reduced by net grant funding of £13m (Q2 2015/16: £62m) mainly relating to our activity on the Broadband Delivery UK (BDUK) programme.

Our base-case assumption for take-up in BDUK areas remains at 33%. Under the terms of the BDUK programme, we have a potential obligation to either re-invest or repay grant funding depending on factors including the level of customer take-up achieved. While we have recognised gross grant funding of £34m (Q2 2015/16: £90m) in line with network build in the quarter, we have also deferred £21m (Q2 2015/16: £28m) of the total grant funding to reflect higher take-up levels on a number of contracts. To date we have deferred £292m.

Free cash flow

Net cash inflow from operating activities was up £489m at £1,734m. Normalised free cash flow1 was up £325m at £894m. The increases primarily reflect growth in EBITDA and timing of receipts and payments in the year.

The net cash cost of specific items was £62m (Q2 2015/16: £30m). This includes EE integration cost payments of £15m (Q2 2015/16: £8m EE acquisition-related cost payments). After specific items and a £44m (Q2 2015/16: £46m) cash tax benefit from pension deficit payments, reported free cash flow was an inflow of £876m (Q2 2015/16: £585m).

Net debt and liquidity

Net debt was £9,573m at 30 September 2016, a reduction of £6m since 30 June 2016 and £272m lower than at 31 March 2016. In the quarter, reported free cash flow of £876m and proceeds of £56m from the exercise of employee share options were offset by payments of £948m on dividends and £30m on our share buyback programme. This quarter we acquired 7.3m shares. Since 1 April 2016 we have acquired 46.9m shares and have spent £206m which completes our share buyback programme, in line with our expectation to spend around £200m this year.

At 30 September 2016 the group held cash and current investment balances of £3.0bn. We renegotiated our £2.1bn committed facility which has been extended by one year to September 2021. In July we repaid the £181m outstanding on the EE acquisition facility. Term debt of £1.4bn is repayable during the remainder of 2016/17. Short term borrowings of £0.9bn also include the outstanding portion of the overdraft facility and collateral for open mark-to-market positions.

On 5 July, S&P upgraded its credit rating on BT from BBB to BBB+ with a stable outlook. We are now rated BBB+ or equivalent with all three of the major credit agencies.

Pensions

The IAS 19 net pension position at 30 September 2016 was a deficit of £9.5bn net of tax (£11.5bn gross of tax), compared with £6.2bn (£7.6bn gross of tax) at 30 June 2016. The increase in the deficit primarily reflects the significant fall in the real discount rate which during the quarter reduced from negative 0.05% to negative 0.87%, its lowest reported level, and the reduction in the assumption for the gap between RPI and CPI. This was partly offset by asset growth.

A large part of the fall in the real discount rate, due to both falling corporate bond yields and higher expected inflation, arose around the time of the Bank of England’s announcement (on 4 August) of the new Quantitative Easing stimulus package, which included plans to purchase £10bn of sterling-denominated investment-grade corporate bonds and £60bn of government debt.

The planning for the triennial valuation, which takes place as at 30 June 2017, is currently ongoing. On a similar timeframe as previous reviews, the valuation would complete in the first half of calendar year 2018.

1 Before specific items, pension deficit payments and the cash tax benefit of pension deficit payments

Regulation

On 4 October 2016, we and other stakeholders submitted responses to Ofcom's proposals for strengthening Openreach’s strategic and operational independence. We remain of the view that our own proposals for significant governance change provide every benefit that Ofcom is seeking while avoiding extensive, disproportionate costs. We will continue to engage with Ofcom over the coming months.

The current charge controls set by Ofcom for the fixed access markets will expire on 31 March 2017. Ofcom is currently undertaking a review of these markets, but does not expect this to be complete by that date. In order to provide certainty to our customers and the wider industry, on 4 August 2016 we provided Ofcom with a commitment to maintain a cap on the relevant price baskets of CPI-CPI until 31 December 2017, or the conclusion of Ofcom's review if earlier.

Dividends

In line with our full year outlook for at least 10% growth in dividend per share, the Board has declared an interim dividend of 4.85p per share, up 10%, and totalling £482m (Q2 2015/16: £368m). It will be paid on 6 February 2017 to shareholders on the register on 30 December 2016. The ex-dividend date is 29 December 2016. The election date for participation in BT’s Dividend Investment Plan in respect of this dividend is 30 December 2016. The final dividend for the year to 31 March 2016 of 9.6p, amounting to £954m, was approved at the Annual General Meeting on 13 July 2016 and paid 5 September 2016.

Outlook

Our outlook is unchanged.

We continue to expect growth in underlying revenue1 excluding transit adjusted for the acquisition of EE in 2016/17. Adjusted EBITDA is expected to be around £7.9bn, after a net investment of around £100m in launching handset offerings to BT mobile customers. Normalised free cash flow is expected to be £3.1bn–£3.2bn. This is after up to £300m of upfront capital expenditure in the Emergency Services Network (ESN) contract, as well as around £100m of EE integration capital expenditure.

For 2017/18, we expect growth in underlying revenue excluding transit and adjusted EBITDA. We also expect to incur capital expenditure of around £100m on the ESN contract and around £100m again on integration. We are confident in our cash flow generation, as a result of the investments we are currently making, the ability of our business to respond to a dynamic industry environment, and ongoing cost transformation and synergy realisation opportunities. As such, we expect to generate normalised free cash flow of more than £3.6bn in 2017/18.

We expect to grow our dividend per share by at least 10% in both 2016/17 and 2017/18. We’ve completed our share buyback programme having bought £206m of shares in 2016/17 to help counteract the dilutive effect of all-employee share option plans maturing in the year. This is below the £315m buyback we completed in 2015/16 reflecting the lower number of shares required for our share option plans.

1Excludes specific items, foreign exchange movements and disposals and is calculated as though EE had been part of the group from 1 April 2015. This differs from how we usually adjust for acquisitions as explained on page 3

GROUP RESULTS FOR THE HALF YEAR TO 30 SEPTEMBER 2016

Note: The results for the period include EE which we acquired on 29 January 2016. Unless referred to as underlying adjusted for the acquisition of EE, the comparatives do not include EE as explained in the notes on page 3.

Income statement

Reported revenue was £11,782m, up 34%. Adjusted revenue, which is before specific items, was £11,828m, up 37%, mainly as a result of the contribution of EE. This includes a £201m favourable impact from foreign exchange movements, and a £16m reduction in transit revenue. Underlying revenue1 excluding transit adjusted for the acquisition of EE was up 0.8%. This reflects growth in Consumer and Global Services, which was partly offset by declines in Business and Public Sector and Wholesale and Ventures.

Reported operating costs were up 39% and adjusted operating costs2 were up 41% at £8,122m, due mainly to EE. Net labour costs of £2,449m were up 16%, reflecting the additional EE employees that joined the group as well as leaver costs of £54m. Underlying operating costs1,2 excluding transit adjusted for the acquisition of EE were up 1%.

Property and energy costs were up 23%, network operating and IT costs up 52% and payments to telecommunications operators up 29%, driven primarily by EE. BT Sport programme rights charges were up 54% mainly as a result of UEFA rights charges. Other costs were up £1,326m or 82%, primarily reflecting EE.

Adjusted EBITDA of £3,706m was up 28%. Underlying EBITDA1 adjusted for the acquisition of EE was down 0.4%. Depreciation and amortisation of £1,724m was up 38% largely due to the impact of EE. Reported net finance expense was £405m while adjusted net finance expense was £300m, up £56m primarily due to higher net debt as a result of our acquisition of EE.

Reported profit before tax (which includes specific items) was £1,388m, up 9%. Adjusted profit before tax increased 20% to £1,675m. The effective tax rate on profit before specific items was 17.9% (HY 2015/16: 18.6%).

Reported EPS (which includes specific items) was 11.6p, down 6%. Adjusted EPS was 13.8p, up 1%. These are based on a weighted average number of shares in issue of 9,933m (HY 2015/16: 8,334m).

Specific items

Specific items resulted in a net charge after tax of £221m (HY 2015/16: £103m). This includes a write down in the value of items on the BT Italia balance sheet of £145m. Other specific items reflect EE integration costs of £46m (HY 2015/16: EE acquisition-related costs £15m), net interest expense on pensions of £105m (HY 2015/16: £111m), property rationalisation costs of £5m (HY 2015/16: £nil) and a profit on disposal of a business of £14m (HY 2015/16: £nil). We also recognised £6m (HY 2015/16: £160m) of both transit revenue and costs, with no EBITDA impact, being the impact of ladder pricing agreements relating to previous years. The tax credit on specific items was £23m (HY 2015/16: £23m). We also recognised a tax credit of £43m for the re-measurement of deferred tax balances due to the UK corporation tax rate reduction (18% to 17%) effective from 1 April 2020.

Capital expenditure

Capital expenditure was £1,579m (HY 2015/16: £1,287m) after £40m (HY 2015/16: £65m) of net grant funding mainly relating to the BDUK programme.

Free cash flow

Net cash inflow from operating activities was up £1,533m at £3,068m. Normalised free cash flow3 was up £667m at £1,342m. The increase primarily reflects growth in EBITDA and timing of receipts and payments in the year.

The net cash cost of specific items was £114m (HY 2015/16: £82m). This includes EE integration cost payments of £33m (HY 2015/16: £24m EE acquisition-related cost payments). After specific items and an £88m (HY 2015/16: £115m) cash tax benefit from pension deficit payments, reported free cash flow was an inflow of £1,316m (HY 2015/16: £708m).

Principal risks and uncertainties

A summary of the group’s principal risks and uncertainties is provided in Note 11.

1 Excludes specific items, foreign exchange movements and disposals and is calculated as though EE had been part of the group from 1 April 2015. This differs from how

we usually adjust for acquisitions as explained on page 3

2 Before depreciation and amortisation

3 Before specific items, pension deficit payments and the cash tax benefit of pension deficit payments

OPERATING REVIEW

Consumer

Revenue was up 11% with a 17% increase in broadband and TV revenue and a 7% increase in calls and lines revenue partly due to the timing of price changes in the period. Consumer 12-month rolling ARPU increased 9% to £38.8 per month driven by broadband, BT Sport Europe and BT Mobile.

Across BT we added 76,000 retail broadband customers, representing 65% of the DSL and fibre broadband market net additions. Superfast fibre broadband growth continued with 216,000 retail net additions, taking our customer base to 4.5m. Of our broadband customers, 49% are now on fibre. Across BT we added 63,000 TV customers, growing our total TV base to 1.7m.

As part of our commitment to improve customer experience by answering 90% of Consumer customers’ calls from within the UK by the end of March, we’ll be adding over 1,000 UK-based customer services roles which will impact costs in the second half of the year. We’re now fixing our customer voice faults on average one day sooner and our average customer broadband speeds have increased by more than 18% compared to the same period last year.

We continue to expand our BT Mobile offering. Last week we launched our Family SIM service, allowing households to easily control their mobile bills in one payment plan. The more SIMs a household takes, the better discount they receive. Households can get up to five SIMs for their mobile and tablet devices, each with their own data allowances.

BT Sport’s average audience figures increased 1% excluding Showcase and digital channels, despite overlapping with coverage of the Olympic and Paralympic games. We’ve seen a strong start to the Premier League season with audiences up. And a UFC contest between Diaz and McGregor in August achieved the highest audience for non-football content in BT Sport’s history.

Since bringing BT and EE together, we’ve been looking at ways we can offer customers the best of each brand. EE customers have already been able to enjoy an introductory period of free BT Sport on their mobile. And we’re now trialling the sale of BT broadband and TV products in 20 EE stores in the UK.

Operating costs increased 8%, a smaller increase than in recent quarters, as last year included BT Sport Europe launch costs. When combined with the ARPU growth, EBITDA increased 23% in the quarter. Depreciation and amortisation was down 10% and operating profit was up 36%.

Capital expenditure was down 5% and operating cash flow increased 61% as a result of our EBITDA growth.

1Restated, see Note 1 to the condensed consolidated financial statements

EE

Revenue was £1,277m, reflecting postpaid mobile revenue of £1,038m, prepaid mobile revenue of £105m, fixed broadband revenue of £69m and equipment sales of £65m. Boosted by strong data roaming revenue, underlying revenue2 adjusted for the acquisition of EE was flat and was up 3% excluding the negative impact of around £30m from regulation.

At the end of the quarter the total BT mobile base was 30.2m. We added 280,000 postpaid mobile customers, taking the postpaid base to 16.4m. EE contributed almost half of these additions. EE postpaid churn was 1.0% reflecting the high level of customer loyalty. The number of prepaid customers reduced by 325,000, in line with industry trends, taking the base to 7.6m. The 4G customer base reached 17.6m. Monthly mobile ARPUs3 were £27.4 for postpaid customers, and £4.4 for prepaid customers.

We continue to work towards our rollout of 4G geographic coverage to 92% of the UK by September 2017 and 95% by the end of December 2020. As at 30 September EE’s 4G coverage reached 70% of the UK’s landmass (98% 4G population coverage), the widest of any UK operator. EE continues to be recognised as the UK’s leading mobile network by RootMetrics, winning its bi-annual Best UK network award for the sixth consecutive time. And EE won the overall award in OpenSignal and Which?’s latest 'State of the UK Mobile Network' report, published in October.

We started the next phase of our 4G+ network, which allows for real world speeds of over 360Mbps, to be deployed on 500 sites across the UK by the end of 2017. Our solution for the Emergency Services Network remains on schedule for delivery in September 2017. Service testing has started in the EE labs and coverage is being expanded by both upgrading existing and building new sites, including the recent switch-on of 4G on the remote Scottish island of Coll.

We remain focused on improving customer experience. Since July we’ve answered 100% of EE postpaid calls in UK and Ireland contact centres, and we continue to make progress towards our goal of handling all EE calls in the UK and Ireland by the end of December.

As part of our ‘more for more’ pricing strategy we introduced a three-tier handset pricing structure, offering our customers increased choice and flexibility. EE Essential plans give access to 4G speeds of up to 20Mbps; 4GEE plans offer unlimited UK minutes and texts and 4G speeds of up to 60Mbps; and 4GEE Max plans combine the largest data bundles, inclusive access to the BT Sport App and ‘roam like home’ voice, text and data usage when abroad in the EU. We also started to offer six months of free Apple Music for new and upgrading EE postpaid customers. In October we announced EE as the exclusive network partner for Google’s first mobile devices in the UK, the Pixel and Pixel XL.

Operating costs were £995m resulting in EBITDA of £282m. Underlying EBITDA2 adjusted for the acquisition of EE was down 1%, reflecting the increased cost of investment in the latest range of devices including the iPhone7. This increased cost is expected to continue into the third quarter. Depreciation and amortisation was £199m.

Capital expenditure was £149m. Adjusted for the acquisition of EE4, capital expenditure was up 17% due to the Emergency Services Network rollout. Operating cash flow was £135m.

1 No comparative information is shown as EE was acquired by BT on 29 January 2016. Note that these are not the results of EE Limited; see Note 1 to the

condensed consolidated financial statements

2 Excludes specific items, foreign exchange movements and disposals and is calculated as though EE had been part of the group from 1 April 2015

3 Consistent with EE Limited ARPU calculation and excludes Consumer mobile customers, who are included in the Consumer ARPU calculation

4Includes EE’s historical financial information as though it had been part of the group from 1 April 2015, under the new organisational structure

Business and Public Sector

Revenue was up 15% mainly reflecting the revenue generated from the SME and corporate customers acquired with EE. Underlying revenue2 excluding transit adjusted for the acquisition of EE was down 7%, due to the ongoing completion of a number of public sector contracts.

Public Sector and Major Business revenue was down 10% for the quarter, with the inclusion of EE revenue more than offset by the decline in public sector revenue. The public sector remains a challenging environment, and we still expect to see headwinds from the completion of contracts in this market for this year and next, as we said at our Capital Markets Day in May.

Corporate revenue increased 55% and SME revenue was up 44%, due to the addition of EE customers. Corporate benefited from continued growth in calls and lines ARPU, while in SME we saw an increase in revenue from IP lines, partly offset by a decline in traditional switch revenue. The higher revenue in each was also driven by growth in mobile, with strong demand for new handsets expected to drive higher acquisition costs going forward.

Foreign exchange movements had a £16m positive impact on Republic of Ireland revenue in the quarter, where underlying revenue2 excluding transit was down 15% mainly due to a large one-off equipment sale in the prior year.

We’ve doubled the speed of BT Infinity for business customers, migrating existing connections to our new standard download speed of up to 76Mbps where technically possible. This will allow our customers to share their broadband with more users, work faster and be more efficient.

Order intake in the quarter decreased 14% to £847m despite the inclusion of EE orders, due to the public sector market conditions as well as a large deal signed in the prior year. On a rolling 12-month basis order intake was down 17% to £3,095m.

We extended our contract with the Co-operative Group to upgrade their MPLS network and roll out secure wi-fi to their 3,000 retail stores, helping the company transform their network infrastructure to future-proof their business and support their in-store innovation programme.

Operating costs increased 12% as a result of EE and EBITDA increased 21% for the quarter. Underlying EBITDA2 adjusted for the acquisition of EE was down 5%, reflecting the revenue decline in the public sector. Depreciation and amortisation was up £19m and operating profit grew 19%, driven by the impact of EE.

Capital expenditure increased £18m. Adjusted for the acquisition of EE3, this was up £5m. Operating cash flow was £52m higher reflecting the £66m increase in EBITDA partly offset by the timing of working capital movements.

1 Restated, see Note 1 to the condensed consolidated financial statements

2 Excludes specific items, foreign exchange movements and disposals and is calculated as though EE had been part of the group from 1 April 2015

3 Includes EE’s historical financial information as though it had been part of the group from 1 April 2015, under the new organisational structure

Global Services

Revenue was up 16% including a £137m positive impact from foreign exchange movements and a £6m increase in transit revenue. Underlying revenue2 excluding transit adjusted for the acquisition of EE was up 3%. Underlying revenue2 excluding transit adjusted for the acquisition of EE was up 9% in the UK driven by large one-off equipment sales and particularly strong IP Exchange volumes. In Continental Europe underlying revenue2 excluding transit was up 1%. In the Americas3 underlying revenue2 declined 3% reflecting the ongoing impact of a major customer insourcing services and in AMEA4 underlying revenue2 was up 5%.

Total order intake was £1.5bn in the quarter, up 10%. On a rolling 12-month basis it was £5.1bn, down 7% year on year. We signed a new contract with Randstad to build a new global IT infrastructure providing cloud connectivity to more than 3,500 sites across 37 countries. We renewed the scope of our global outsourcing contract with Unilever, including connectivity, regional data centre and unified communications services delivered to more than 700 sites across 96 countries. We signed a new contract with one of the largest banking groups in Spain, Banco de Sabadell, to provide a range of managed network services. This enables them to support their operations in the UK following its acquisition of TSB. And we extended our contract with Bristol-Myers Squibb for the provision of outsourced networked services covering more than 100 sites across 50 countries.

We continued to execute our Cloud of Clouds portfolio strategy with the launch of BT Compute for Microsoft Azure, a solution that allows BT customers to order integrated cloud services from Microsoft alongside BT’s own cloud services.

We’ve also completed integration of the next generation of security products from Palo Alto Networks and Fortinet into our managed security services. These provide customers with advanced protection capabilities to address the ever increasing cyber threats that our customers face. And for the Rio Olympics we provided an enhanced denial of service protection capability in support of key customers requiring additional security. We announced a three-year plan for new investments in Latin America including new network points of presence and integration of the latest security features to help our customers expand in the region.

Operating costs increased 16%, mainly reflecting the impact of foreign exchange movements. Underlying operating costs2 excluding transit adjusted for the acquisition of EE were up 4% reflecting the impact of higher revenue in the quarter. EBITDA increased 17% whilst underlying EBITDA2 adjusted for the acquisition of EE was flat. Depreciation and amortisation was up 7% and operating profit was £24m.

Capital expenditure was up 3% and operating cash flow was £58m.

1 Restated, see Note 1 to the condensed consolidated financial statements

2 Excludes specific items, foreign exchange movements and disposals and is calculated as though EE had been part of the group from 1 April 2015

3 United States & Canada and Latin America (Americas)

4 Asia Pacific, the Middle East and Africa (AMEA)

n/m = not meaningful

Wholesale and Ventures

Revenue was down 9% with underlying revenue2 excluding transit adjusted for the acquisition of EE down 5% as a result of the decline in Partial Private Circuits and call volumes.

Managed Solutions revenue was down 40%, broadly in line with the decline in the first quarter, as last year included revenue from contracts with EE which is no longer recognised, given the acquisition and reorganisation of EE within the group.

Data and Broadband revenue was down 5%. Again this was largely as services provided to EE are no longer recognised as revenue. The decline was also due to Partial Private Circuits customers continuing to move onto newer Internet Protocol (IP) based technologies. Broadband revenue grew again as we continue to drive take-up of fibre in the market. And Ethernet delivered another good quarter with a 17% increase in the rental base to 41,500. In July we launched a new platform which makes it quicker and easier for our customers to order Ethernet circuits online.

Voice revenue was down 28%. This reflected ongoing declines in call volumes, and that last year benefited from EE revenue which is no longer recognised given the acquisition and reorganisation of EE within the group.

Mobile generated revenue of £54m, in line with the first quarter, with most of this coming from EE’s MVNO business which is now reported within Wholesale and Ventures.

Our Ventures business generated revenue of £82m. This was above the first quarter, mainly driven by our phonebook business.

Order intake of £302m was down 12% on last year and was £1,355m on a rolling 12-month basis. In July, our Media and Broadcast business completed work upgrading 20 leading football stadiums around the UK with an ultrafast fibre network. 40Gbps of fibre capacity will run directly from each Premier League football ground to the BT Tower, delivering live footage of matches to both national and global audiences.

Operating costs decreased 21% and EBITDA increased 17%. Underlying EBITDA2 adjusted for the acquisition of EE was down 2%. Depreciation and amortisation increased 19% and operating profit increased 15%.

Capital expenditure was £51m, broadly in line with the first quarter and the prior year, and operating cash flow was £155m.

1 Restated, see Note 1 to the condensed consolidated financial statements

2 Excludes specific items, foreign exchange movements and disposals and is calculated as though EE had been part of the group from 1 April 2015

Openreach

Revenue was flat with regulatory price reductions having a negative impact of around £60m, the equivalent of around 5% of revenue. This impact of regulation was offset by 37% growth in fibre broadband revenue.

We continue to extend the reach of fibre broadband beyond our commercial footprint as part of the BDUK programme. We passed around 300,000 properties in the quarter which means our superfast fibre broadband network is now available to 26m premises.

The UK broadband market2 grew by 116,000 connections compared with 160,000 in the prior year while the physical line base reduced by 42,000. We achieved 440,000 fibre broadband net connections, taking the number of homes and businesses connected to our fibre broadband network to 6.7m, 26% of those passed. Service providers other than BT added 224,000 or 51% of the total net connections in the quarter, demonstrating the market-wide demand for fibre.

We’re trialling a new technology, Long Reach VDSL, to increase the speed of fibre broadband over long lines. We believe this could benefit rural areas and in the quarter we added remote communities on the Isle of Lewis in Scotland to this service. We plan to add further trial locations of the technology from January. Our G.fast pilots are progressing well and will soon be extending to 12 further locations, making G.fast available to 140,000 customers across 17 locations. This, along with our expanding FTTP footprint, means we’ll be able to offer ultrafast broadband to 500,000 homes and businesses by April 2017.

Operating costs grew 4%. This partly reflects the cost of starting to clear a long tail of outstanding Ethernet orders, including the cost of service level guarantee payments, which we expect to continue into the second half. We also continue to invest in customer experience and remain on track to halve missed appointments by the end of this financial year. We’re ahead on all 60 minimum service levels set by Ofcom. EBITDA was down 2% and depreciation and amortisation was 1% up, resulting in operating profit down 6%.

Capital expenditure was £357m, up £9m or 3%. This was after gross grant funding of £34m (Q2 2015/16: £87m) directly related to our activity on the Broadband Delivery UK (BDUK) programme build in the quarter. This was offset by the deferral of £21m of the total grant funding (Q2 15/16: £26m). We continue to expect gross capital expenditure in 2016/17 to be higher than in the previous year.

Operating cash flow increased 39% largely due to the timing of customer receipts.

1 Restated, see Note 1 to the condensed consolidated financial statements

2 DSL and fibre, excluding cable

We will hold the second quarter and half year 2016/17 results presentation for analysts and investors in London at 9.00am today and a simultaneous webcast will be available at www.bt.com/results

We are scheduled to announce the third quarter results for 2016/17 on Friday 27 January 2017.

Topics

- Sport

Categories

- shareholders

- financial results

About BT

BT’s purpose is to use the power of communications to make a better world. It is one of the world’s leading providers of communications services and solutions, serving customers in 180 countries. Its principal activities include the provision of networked IT services globally; local, national and international telecommunications services to its customers for use at home, at work and on the move; broadband, TV and internet products and services; and converged fixed-mobile products and services.BT consists of six customer-facing lines of business: Consumer, EE, Business and Public Sector, Global Services, Wholesale and Ventures, and Openreach.

For the year ended 31 March 2016, BT Group’s reported revenue was £19,042m with reported profit before taxation of £3,029m.

British Telecommunications plc (BT) is a wholly-owned subsidiary of BT Group plc and encompasses virtually all businesses and assets of the BT Group. BT Group plc is listed on stock exchanges in London and New York.

For more information, visit www.btplc.com

BT News