Nyhet -

In Focus: the eurozone's current inflation

The eurozone’s current inflation rate is above the ECB’s desired level. However, further policy easing should still be possible in order to support the weak regional economy given the moderating trend of inflation and given that inflation expectations appear well anchored.

Although still above the ECB’s 2.0% target rate, since the start of the year, inflation in the eurozone has exhibited a moderate declining trend. Moreover, with inflation expectations considered to be under control and the eurozone’s economy still under stress, further cuts to the ECB’s main policy interest rate may be possible in the coming months.

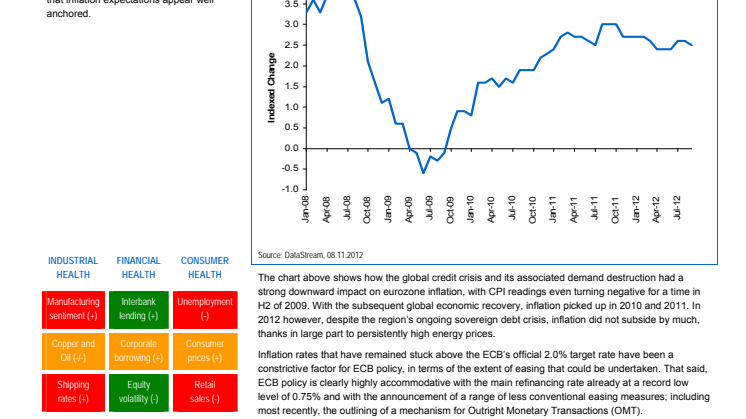

With the subsequent global economic recovery, inflation picked up in 2010 and 2011. In 2012 however, despite the region’s ongoing sovereign debt crisis, inflation did not subside by much, thanks in large part to persistently high energy prices. Inflation rates that have remained stuck above the ECB’s official 2.0% target rate have been a constrictive factor for ECB policy, in terms of the extent of easing that could be undertaken. That said, ECB policy is clearly highly accommodative with the main refinancing rate already at a record low

level of 0.75% and with the announcement of a range of less conventional easing measures; including most recently, the outlining of a mechanism for Outright Monetary Transactions (OMT). Looking ahead, further policy easing should be possible in the coming months. The main reasons for this are: 1) although somewhat above the ECB’s desired level, inflation has been on a moderate declining trend in the past few months, with the ECB also believing that broader inflation expectations are ‘well anchored’; and 2) the continuing weakness of the eurozone economy with early signs that this weakness is spreading to the once distinctively robust-looking German economy.

This information is for Investment Professionals only and should not be relied upon by private investors. It must not be reproduced or circulated without prior permission. This communication is not directed at, and must not be acted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. Fidelity/Fidelity Worldwide Investment means FIL Limited and its subsidiary companies. Unless otherwise stated, all views are those of Fidelity. Fidelity only offers information on its own products and services and does not provide investment advice based on individual circumstances. Fidelity, Fidelity Worldwide Investment, the Fidelity Worldwide Investment logo and F symbol are trademarks of FIL Limited. Growth Investments Limited is licensed by the MFSA. Fidelity Funds are promoted in Malta by Growth Investments Ltd in terms of the EU UCITS Directive and Legal Notices 207 and 309 of 2004.The Funds are regulated in Luxembourg by the Commission de Surveillance du Secteur Financier; Our legal representative in Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich. Paying agent for Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich.Issued by FIL Investments International (FSA registered number 122170) a firm authorised and regulated by the Financial Services Authority. FIL Investments International is a member of the Fidelity Worldwide Investment group of companies and is registered in England and Wales under the company number 1448245. The registered office of the company is Oakhill House, 130 Tonbridge Road, Hildenborough, Tonbridge, Kent TN11 9DZ, United Kingdom. Fidelity Worldwide Investment’s VAT identification number is 395 3090 35 IC12/85

Ämnen

- Finans

Kategorier

- fidelity

- fidelity international

- fidelity worldwide investment

- eurozone

- inflation