Blog post —

EU VAT changes: Twitter Q & A

VAT place of supply of services rules change from 1 January 2015. HM Revenue and Customs (HMRC) held a Twitter Q & A on 27 November 2014. Here we list some of the main questions and answers to come out of that.

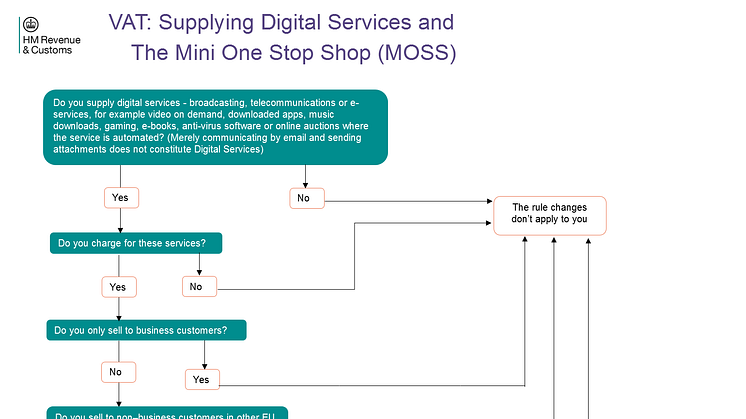

Section A: What is a digital service?

A1 What constitutes a digital service? #VATMOSS

A. You can find some explanation about that here: https://www.gov.uk/vat-on-digital-services-in-the-.... #VATMOSS

A2 What constitutes an e-service? #VATMOSS

An e-service is one that is fully automated and involves no or minimal human intervention. #VATMOSS

A3 What do you mean by “minimum human intervention”? #VATMOSS

Please see examples at Annex A.

A4 Does #VATMOSS apply to web hosting, SAAS, cloud storage, analytics, online accounting, remote maintenance and web advertising? #VATMOSS

Yes if those services are automated and involve no, or minimal, intervention. #VATMOSS

A5 Does this mean I need to be VAT registered to sell ebooks? #VATMOSS

If you sell ebooks to consumers in other member states through own fully automated website this will be an e-service, so yes. #VATMOSS

A6 If I run a paid live webinar (human interaction) and have a free pdf download with it, is that liable under #VATMOSS?

No, the live webinar is not an e-service and the pdf download, provided it is genuinely free, will not be affected by new rules. #VATMOSS

A7 Is delivering part live, part downloadable content to customers around the EU exempt from #VATMOSS?

Live content not an e-service, downloadable content is. Depends on which part of transaction was principal element for customer. #VATMOSS

A8 If I have paid membership for my website and people can then get free online courses, is that a digital services under #VATMOSS?

If course is fully automated it’s an e service. If there is “human intervention” eg online tutors, live Q&As etc, it’s not. #VATMOSS

A9 What about virtual classrooms combining live webinars, videos, pdfs & human intervention? #VATMOSS

A virtual classroom combining all these elements would not be an e-service because of the amount of human intervention involved. #VATMOSS

A10 What if an e-course contains recorded videos & PDFs but is opened at specific times only + has live interaction? #VATMOSS

The inclusion of live interaction means that this is not an e-service. #VATMOSS

A11 If I offer coaching (human intervention) with an online course, how do I handle that to comply with #VATMOSS?

The inclusion of live coaching means that this is not an e service. #VATMOSS

A12 Is a PC software license a digital service?

Yes, if supplied automatically as a download #VATMOSS

A13 We offer software bundle download + DVD mail order. Where and how do we account for VAT on bundle - UK or EU country?

Depends on the principal element. If DVD it will be a supply of goods; if software it will be an e service #VATMOSS

Section B: Why no minimum threshold on cross-border digital supplies?

B1 Why are these changes coming into effect? #VATMOSS

To create a level playing field for all businesses so supplies are taxed where consumed and to protect tax revenues. #VATMOSS

Businesses that have moved offshore to low tax or no tax jurisdictions will no longer be able to undercut UK businesses on tax. #VATMOSS

B2 Why can't there be a minimum VAT threshold like in UK? #VATMOSS

Within limits, each Member State decides on its own VAT threshold, and we cannot impose our threshold on them. #VATMOSS

B3 Why isn’t there an EU wide digital services threshold?

Many Member States are opposed because of their low domestic VAT thresholds and they consider it would undermine their small businesses. #VATMOSS

Section C: Sales via third-party platforms

C1 What constitutes a marketplace? #VATMOSS

A simple definition is that if a marketplace is responsible for authorising/allowing the download it is responsible. #VATMOSS

C2 But many/most digital content providers trade through their own websites, not just e-marketplaces? #VATMOSS

These providers will have to consider options. But if they can separate into UK & non-UK businesses they can use #VATMOSS.

C3 Can you clarify the platform tip? Are *ALL* platforms including @Etsy @paypaluk @folksy responsible without exception? #VATMOSS

They are responsible if they authorise the download or payment process or set T&Cs. #VATMOSS

C4 So if I use PayPal as my payment platform I don't have to worry about #VATMOSS?

Paypal provides payment mechanism; it does not take part in supply of services so it is not responsible for accounting for VAT. #VATMOSS

C5 If microbusinesses use PayPal buttons on their site for digital products, can we assume #VATMOSS will be covered by PayPalUK?

No. PayPal is not an e-marketplace. It is a 3rd party payment provider. #VATMOSS

C6 So which platforms will take responsibility and which will leave us to do it ourselves?

We are referring to platforms where order is placed, payments are processed and delivery made through its website. #VATMOSS

C7 Many crafts sell digital services direct through platforms that can rebut the criteria, and won't deal with #VATMOSS for us.

We have not received a credible rebuttal to date, as all these platforms are responsible for authorising the download. #VATMOSS

C8 Re platforms, I don't think HMRC and EU realise that not all platforms handling digital sales have European presence. #VATMOSS

Platforms with no EU presence will be required to account for VAT in exactly the same way as EU businesses. #VATMOSS

C9 How will #VATMOSS interact with things like Patreon and Kickstarter pledges, where people are rewarded for donations?

It depends on the nature of the reward #VATMOSS

Section D: VAT Registration and MOSS

D1 If I am not VAT registered in UK will I be able to register for MOSS?

No, you need to be VAT registered. But if you separate the cross-border business you can voluntarily register that for VAT and MOSS #VATMOSS

D2 What about UK sellers for whom digital sales are a small part of their business? #VATMOSS

If you can separate the part of your business which makes cross-border digital services… #VATMOSS 1/3

…You may voluntarily register that part of business for VAT in UK. This will enable you to then register for MOSS in UK. #VATMOSS 2/3

..HMRC is currently preparing detailed guidance for businesses on this issue #VAT MOSS 3/3

D3 Do you really recommend two businesses to help with #VATMOSS? Usually you call that revenue splitting?

It is not, because the UK biz is still below the UK limit. It is not an artificial split to avoid UK VAT registration or paying VAT. #VATMOSS

D4 Re single entity and disaggregation, is HMRC saying special concession is being/will be offered for providers of digital services? #VATMOSS

No. This is a normal application of the rules not a special concession or derogation. #VATMOSS

It simply recognises digital services biz will not be seeking to avoid UK VAT or engaging in unfair competition with other UK biz. #VATMOSS

D5 Are there any legal issues if a UK website decides not to sell to customers in the EU (including fellow UK.)?

Not for VAT but other legislation (eg anti discrimination) may apply #VATMOSS

D6 If I can't buy software critical to my microbusinesses after Jan 1st by download how can I legally work around?

As a buyer the new rules will not affect you #VATMOSS

D7 Do you have to become VAT Reg here in the UK if UK t.o. Under £81k & account for vat on UK sales to use #VATMOSS?

No, you need to be VAT registered. But if you separate the cross-border business you can voluntarily register that for VAT and MOSS #VATMOSS

Section E: Evidence of customer’s location

E1 What evidence do I need to prove customers location?

A30 Two pieces of non-contradictory evidence such as, for example, IP address, bank account address or SIM card identifier code #VATMOSS

E2 We use paypal but don't always get address info - how are we meant to implement changes??

Any two pieces of non-contradictory evidence such as, IP address, bank account address or SIM card identifier code will suffice #VATMOSS

Section F: Admin / keeping records

F1 How can I manage the admin burden of #VATMOSS?

If you are selling through an e-marketplace, then it should deal with the VAT. If not consider MOSS registration #VATMOSS

F2 But what about sole traders selling through own websites? #VATMOSS

If you are making digital sales to customers in other MSs you should already be collecting basic customer info #VATMOSS

F3 How do you propose we capture the information you insist we have for compliance? Are you releasing compliant plugins? #VATMOSS

When consulting with business about changes, feedback was that information is routinely collected, though not always looked at. #VATMOSS

F4 Given that #VATMOSS starts 1st Jan & we need to keep records from 31st Dec in year sale is carried out, that's actually 11 years.

It is, in effect, between 10 and 11 years. #VATMOSS

F5 Personal data should not be kept for longer than necessary." So why keep info on digital product buyers for 10 YEARS? #VATMOSS

10 years is because that is the EU-wide requirement.

F6 How can a one-person sole-trader set up cope with the data storage legal requirements? #VATMOSS

If your sales are not made via e-marketplace (and therefore this does not apply to you) then we suggest archiving the data. #VATMOSS

F7 Very concerned that keeping data for #VATMOSS for 10 yrs means data protection registration for few EU sales.

You do have to comply with current data protection requirements. #VATMOSS

F8 I don't want to hold my digital customers bank account details, IP address and the other reams of info the EU want me too. #VATMOSS

You only need to hold two pieces of non-contradictory evidence. #VATMOSS

Section G Enforcement & Compliance

G1 How will the new rules be enforced? #VATMOSS

Through existing administrative co-operation and information exchange with other fiscs. and compliance activity #VATMOSS

G2 The rules have been in since 2003 for non-EU sellers, e.g USA. I want to know if HMRC are going to enforce this now? #VATMOSS

We always have enforced it and when we identify a biz that should be registered we contact them and get the tax. #VATMOSS

Section H: Additional Help

H1 What help is there for small biz if they do register for VAT and MOSS? Currently no software solutions! #VATMOSS

If a business needs to register for MOSS and VAT then there are online solutions available. Internet search will identify them. #VATMOSS

H2 I need some specific advice relating to my business. What can I do? #VATMOSS

You can email us at vat2015.contact@hmrc.gsi.gov.uk. #VATMOSS

H3 Why are we only finding out about these rules now? #VATMOSS

The changes were agreed 6 years ago and we have been publicising them to UK businesses for several years. #VATMOSS

H4 Who is the appropriate person/body to contact to campaign for removal of the zero VAT threshold on digital sales? #VATMOSS

EU Commission. #VATMOSS

Annex A: What is meant by minimal human intervention?

What constitutes an e-service? #VATMOSS

An e-service is one that is fully automated and involves no or minimal human intervention. #VATMOSS

What is meant by “no human intervention”?

This is where the sale of the digital content is entirely automatic – for example a customer clicks the “Buy Now” button on website and

- the content downloads onto the customer’s device, or

- customer receives automated e-mail containing content.

In both cases these would constitute an e-service.

What is “minimal human intervention”?

This is where the sale of the digital content is mostly automatic but the small amount of manual process involved does not change the nature of the supply from an e-service - for example a customer clicks “Buy Now” button on website and

- vendor receives notification and clicks a button, which produces an email pre-populated with the customer’s details and containing content which is sent to the customer; or

- vendor receives notification and clicks a button which produces an e mail pre-populated with the customer’s details. Vendor attaches content and sends customer e-mail by clicking “Send”

In both cases these would constitute an e-service

When does the “human intervention” exceed “minimal”

This is where the amount of manual process involved in the sale means that the service ceases to be an e-service. In these cases the website functions as a “shop window” for the sale rather than also providing the mechanism by which the sale is made – for example

- a customer clicks “Buy Now” button on website and is added to a list. At end of day the vendor takes list, manually completes an e-mail with each customer’s details, attaches the relevant content and hits “Send”; or

- a customer emails vendor with details of the products they wish to purchase. Vendor manually replies to email and attaches the content.