Press release -

PwC: Small steps for Singapore companies could mean a giant leap for more relevant reporting

PwC: Small steps for Singapore companies could mean a giant leap for more relevant reporting.

Singapore, 23 September 2014 – PwC’s landmark analysis report titled (Towards more relevant reporting) finds that the annual reports of many companies in Singapore already have some components required by the Integrated Reporting (<IR>) framework such as information about strategy, business model and risks, but they would need to link these elements better to holistically communicate a more relevant value creation story to stakeholders.

The analysis, first of its kind in Singapore surveyed the 30 component companies on the STI with 110 questions that include the 7 <IR> content elements - Organisational overview and external environment (OOEE), Governance (Gov), Risk & Opportunities (R&O), Business Model (BM), Strategy and resource allocation (S&RA), Performance (Perf) and Future Outlook (FO). These elements are crucial for a company to communicate value to its various stakeholders.

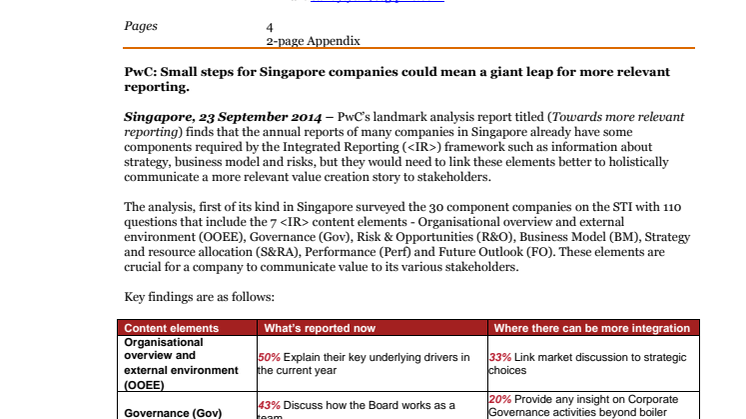

Key findings are as follows:

|

Content elements |

What’s reported now |

Where there can be more integration |

|

Organisational overview and external environment (OOEE) |

50% Explain their key underlying drivers in thecurrent year |

33% Link market discussion to strategic choices |

|

Governance (Gov) |

43% Discuss how the Board works as a team |

20% Provide any insight on Corporate Governance activities beyond boiler plate terms of reference |

|

Risk and opportunities (R&O) |

57% Identify its principal risks |

17% Link risk reporting with other aspects of reporting |

|

Business model (BM) |

63% Make reference to their business model |

3% Measure their value-creating activities |

|

Strategy and resource allocation (S&RA) |

70% Disclose a strategic vision |

10% Integrate its strategies and priorities well into the rest of the annual report |

|

Performance (Perf) |

27% Explicitly identify KPIs |

10% Link KPIs to strategy |

|

Future Outlook (FO) |

20% Discuss future availability and constraints ofmaterial non-financial capital that it relieson to create value |

3% Set out KPIs to measure its impact of the non-financial capitals |

Other key findings include:

1. Most of the STI constituents already disclosed some of the elements set out in the <IR> Framework. In particular, some Singapore companies have started disclosing more information about their strategic priorities, business models and external environments.

2. One of the key observations is that while there were a lot of disclosures, there was a lack of linkage between the information provided. The strength of <IR> lies not in the individual disclosures for each content element but in the interconnectivity between all the content elements to tell an integrated value creation story. DBS, as the first company in Singapore to adopt <IR>, have in addition to disclosing the content elements, also applied the various principles set out in the Framework including connectivity, strategic focus and future orientation.

3. Most companies still tend to have a compliance mindset, such as disclosing boilerplate information to be in line with the requirements or their peers. For example, most companies seem more comfortable to report on board charters and terms of reference rather than the actual activities undertaken by the Board and their effectiveness. The risk disclosures list out the risks but rarely disclose what the company is doing to mitigate them, as well as translating them into opportunities as part of their strategy.

4. Historical and financial reporting remains the focus, with many companies still reluctant to have a more extensive discussion on what the future may hold for them. There is also a lack of discussion around non-financial variables which affects a company’s ability to deliver value.

Said Oon Jin Yeoh, Executive Chairman of PwC Singapore:

“PwC believes in Singapore’s aspiration to be a leading global accountancy hub in Asia Pacific. As such, we have devoted significant resources to analyse the annual reports of the 30 companies comprising the STI to better understand where these leading Singapore companies stand with regards to the <IR> Framework.”

“Integrated Reporting <IR> has the potential to deliver greater trust in reporting through integrated thinking. The framework promotes the breaking down of silos within the organisation to consider its key capitals, its business model and communicate the value creation process to the various stakeholders of the organisation. This helps the organisation to push the boundaries with excellent and innovative reporting beyond a compliance mindset and sets it apart from its peers.

It is encouraging that the Singapore companies analysed are already disclosing some content elements required by <IR>. What is clear from the analysis is that the actual gaps to the <IR> Framework were not as significant as perceived and companies should consider taking steps to start incorporating various content elements and principles in the <IR> Framework.”

Said Paul Druckman, Chief Executive Officer (CEO) of International Integrated Reporting Council:

"This report provides an excellent baseline of corporate reporting in Singapore and sets out a path that will enable businesses to progress their journey. We have seen integrated reporting becoming embedded in Singapore in recent months and have high expectations of a significant shift in the next reporting cycle."

Said Mikkel Larsen, Managing Director, Group Head of Tax and Accounting Policy of DBS Group Holdings Ltd:

“PwC's analysis is insightful on how Singapore companies already have some of these information required by IR in their annual reports and the biggest challenge remains to link these information to better explain the companies' value creation process. The report is also helpful as it provides examples of good reporting and recommendations on how companies can challenge the boundaries of their existing reporting. DBS' own experience is that IR enabled us to better communicate how we were executing against our strategy and creating value to the various stakeholder groups.

It is also important to note that in reality IR is a just framework to promote high quality financial communication but that, it does not mean that all annual reports have to be an integrated report."

Said Mr Lee Fook Chiew, Chief Executive Officer of the Institute of Singapore Chartered Accountants (ISCA):

“We commend this initiative by PwC, which highlights current reporting trends in Singapore, and paves the way for Singapore companies to work towards better corporate reporting. ISCA is pleased to work with PwC and other members of our Integrated Reporting Steering Committee, to reinforce Singapore’s position as a hub for thought leadership in integrated reporting. Working closely with key stakeholders like PwC, ISCA is committed to playing an active role in influencing and shaping the global movement towards better corporate reporting and helping Singapore companies in their integrated thinking and reporting journey.”

Concluded Chen Voon Hoe, Integrated Reporting Leader, PwC Singapore:

“Companies

today spend a significant amount of time preparing their existing financial

reports, but the challenge is always to make the report more relevant to the

readers amidst the perception that it’s too complex, too historical and too

financial focused. The <IR> framework allows companies to make their

reporting more relevant. However, achieving this is not just about providing

more info but about a change in mindset.”

-ENDS-

Notes to editor:

- The International Integrated Reporting Council (IIRC) is a global coalition of regulators, investors, companies, standard setters, the accounting profession and NGOs. Together, this coalition shares the view that communication about businesses’ value creation should be the next step in the evolution of corporate reporting. Integrated Reporting <IR> is “a concise communication about how an organisation’s strategy, governance, performance and prospects, in the context of its external environment, lead to the creation of value over the short, medium and long term.”

- This analysis surveyed the 30 companies constituting the Straits Times Index by conducting a detailed assessment of 110 questions. The 110 questions covered the 7 content elements in the <IR> Framework, and they assessed the quality of the information presented and how well it was integrated throughout the annual report. This research was performed as part of PwC Global initiatives on Integrated Reporting and similar studies were done in other countries around the world such as the United Kingdom, Switzerland, the Netherlands, Malaysia, etc.

Appendix 1 – In-depth analysis of the findings by 7 <IR> elements

1. Organisational overview and external environment

Currently, 50% of Singapore companies surveyed explain their key underlying drivers of market growth well, but do not discuss expected trends of their key drivers in their reports. Only 33% of companies surveyed linked market trends to strategic choices by the company’s management. The survey also found that here was a general lack in discussion on the company’s competitive environment.

PwC Point of View:

With <IR>, Singapore companies can allow readers to better understand their external environment which consist of competitors, customers or market trends that influences its strategic activities and choices. Also, there should be a higher emphasis on providing forward-looking information and quantified industry trends to give readers an idea of how the company can achieve its medium and long term goals.

2. Governance

This is the top element that possesses opportunities for development in reporting. The survey found that 43% of companies surveyed discussed how the Board works as a team but did not share on the actions the Board took to add value to the company. Majority of the companies provided generic boiler plate governance practices. Only a minority 13% linked governance to the rest of the report and showed how it had led the company to make its strategic decisions.

PwC Point of View:

There is a need for Singapore companies to move away from the compliance mindset and provide more insights on the effectiveness of the Board in creating value. In addition, there should be a clear link between the Board’s KPIs and their remuneration packages.

3. Risk and opportunities

Under the category of Risk and Opportunities, the analysis finds that Singapore companies need to steer away from listing a generic list of risks in their reporting. While 57% of the companies identified their principal risks and uncertainties, only 17% linked these risks to other reporting aspects such as strategy and performance.

PwC Point of View:

Companies need to identify the principal risks that may disrupt their business from achieving its strategic objectives. After these risks are identified, measures taken to deal with the risks need to be relayed to the stakeholders. This can be done by disclosing a risk profile diagram.

4. Business model

The findings show that the majority of Singapore companies surveyed (63%) described their business lines with historical narratives on performance. Only an insignificant 10% identified their differentiating and value-creating elements in their business models.

PwC Point of View:

A business model explains what a company does and showcases how it creates value to its stakeholders. However, it is essential to pick out the key differentiating and value-adding activities which set them apart from its peers. Information on measurement of value creating activities by coming up with relevant KPIs are also lacking in current reporting.

5. Strategy and resource allocation

Strategy is the intersection core of all the key elements in a report. Most companies surveyed (70%) made a clear statement about its overall goal or strategy, but only 10% of them integrated their strategies and priorities well into the rest of the annual reports.

PwC Point of View:

It is becoming increasingly important for companies to report their short, medium and longer term priorities and how these respective priorities will result in their overall goals of the company.

6. Performance

The report shows that currently, it is difficult to have a clear understanding of what drives performance in the firm as only a small percentage (27%) of companies disclose their Key Performance Indicators (KPIs). Out of this 27%, only 10% aligned the KPIs with their key strategic priorities. Most companies do not provide insight or measurements towards how the company will continue to be sustainable.

PwC Point of View:

There is an impending need for companies to focus less on the financials and historical performances of the firm and instead, include more non-financial KPIs in reporting. In fact, aligning both financial and non-financial KPIs with strategic priorities will better allow stakeholders to understand the company’s value creation process.

7. Future outlook

A growing number of companies have started to report insights to sustainability issues that their companies have undertaken. However, only 20% of the companies surveyed discussed future availability and constraints of material non-financial capital they rely on to create value. The disclosure of KPIs to measure the sustainability targets is often left missing.

PwC Point of View:

Companies need to broaden their scope on their future outlook and sustainability issues. They need to forecast the external environment and predict factors that may hinder their performance. Once done, they should come up with measures to counter any adverse factors. Although Singapore companies have been increasingly focusing on sustainability, the link with strategy needs to be strengthened. The availability and constraints of key non-financial inputs must not be neglected.

Related links

Topics

Categories

About PwC

PwC helps organisations and individuals create the value they’re looking for. We’re a network of firms in 157 countries with more than 184,000 people who are committed to delivering quality in assurance, tax and advisory services. Tell us what matters to you and find out more by visiting us at www.pwc.com.

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

© 2014 PricewaterhouseCoopers. All rights reserved.